countries included

active extraction areas

areas under development

oil and gas discoveries

Overview

New oil and gas production activity is lower than previous decades but remains out of line with global climate goals.

Scenarios compatible with limiting warming to 1.5°C show that oil and gas demand can be met without developing any new fields, and emissions from existing oil and gas projects push well past remaining carbon budgets for that target. Yet, major producing countries are doubling down to maintain current production levels, while new countries are also looking to extract oil and gas, betting on high carbon futures or risking stranded assets.

As many of the easiest basins for extraction have been thoroughly developed, companies and countries are turning to riskier projects to maintain their production and offset maturing fields. Offshore drilling is becoming more prevalent, more complicated reservoirs are being tapped, and production in frontier regions with large infrastructure costs is being targeted. Lead times for new conventional projects are getting longer, indicating that converting resources into supply has become materially more complex and slower.

Five producers — the United States, Russia, Iran, Canada, Saudi Arabia, and China — produce nearly 60% of the world's oil and gas. These five countries are exploring for new projects in order to maintain their status as top producers. The Oil Majors (ExxonMobil, Shell, Chevron, TotalEnergies, bp, and ConocoPhillips) are exploiting new hydrocarbon resources in countries that historically have not produced much or any oil and gas, potentially creating new petrostates financially invested in the continued use of oil and gas.

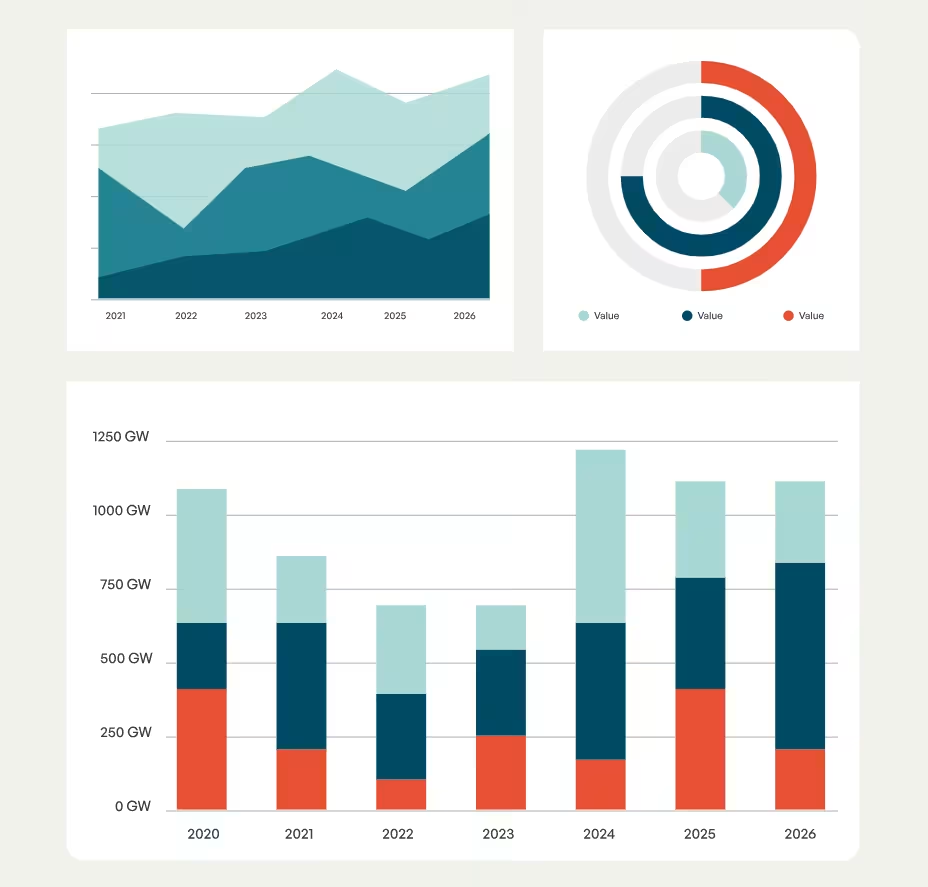

Business as usual production requires annual discoveries of about 16 billion barrels of oil equivalent (boe), according to the International Energy Agency. In 2025, 7 billion boe were discovered, 45% of the discovery volumes called for. Discoveries were in the same range as 2025 throughout the 2020s. The result is structural misalignment: Supply plans are inconsistent with climate goals, yet discovery trends are insufficient to sustain flat production over the long term.

Offshore development now accounts for 29% of global production, with recent projects predominantly offshore.

Russia, Norway, Nigeria, Australia, and the United States hold 34% of pre-production fields.

Meet the team

If you have questions about this project, please contact the Project Manager, Scott Zimmerman.

Get in touch

Related projects

The Global Oil and Gas Plant Tracker is a worldwide dataset of oil- and gas-fired power plants.

The Global Oil Infrastructure Tracker (GOIT) catalogs midstream oil and natural gas liquids transmission pipeline infrastructure, with asset-level dat...

The Global Gas Infrastructure Tracker (GGIT) gathers asset-level data on gas transmission pipeline projects and liquefied natural gas import and expor...

Methodology

Frequently asked questions

Contact

For questions about the Global Oil and Gas Extraction Tracker, contact Scott Zimmerman: