Global Energy Monitor's June 2026 update to the Global Oil Infrastructure Tracker (GOIT) arrives amid the largest supply disruption in the history of the oil market. Even with a deal to reopen the Strait of Hormuz, flows remain a fraction of pre-war levels and the vulnerability is now undeniable.

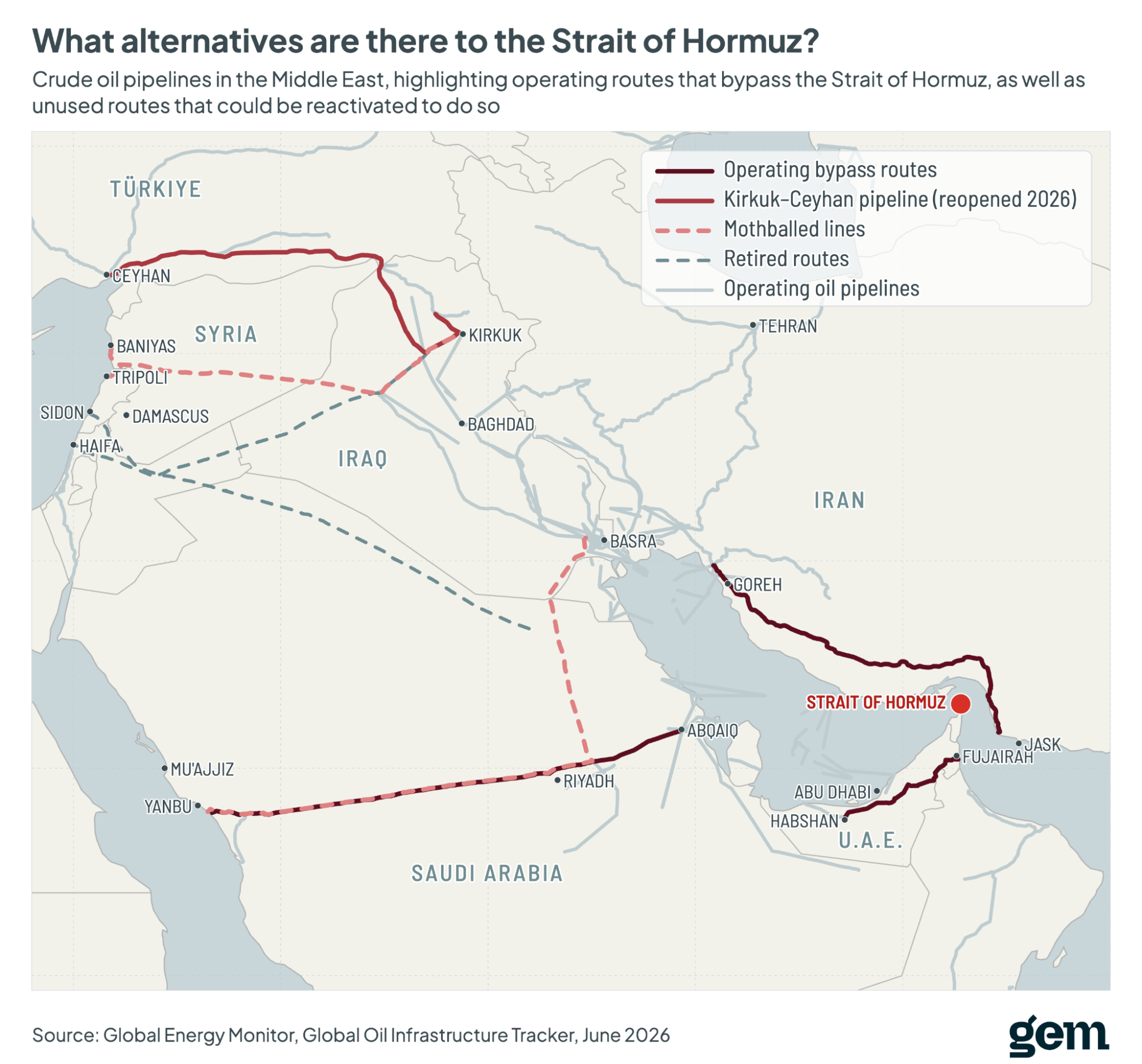

At the start of the crisis, only a handful of operating overland routes could move Persian Gulf crude without transiting Hormuz, including Saudi Arabia's East–West line to the Red Sea, the UAE's Habshan–Fujairah line, and Iran's underused Goreh–Jask route. In March 2026, the Kirkuk–Ceyhan pipeline was reopened after a decade to allow crude exports from Iraq to Türkiye. The data show nearly 3,300 kilometers (km) worth of additional Iraqi export pipelines that are now part of rerouting discussions. These include the IPSA line, the Kirkuk–Baniyas corridor, and the Kirkuk–Tripoli route. Finally, two retired pipelines have been mentioned — the Tapline and Kirkuk–Haifa — but there are no serious proposals to reopen them.

These routes are a reminder of how much the global economy leans on a handful of vulnerable corridors and the challenge in rerouting major crude oil flows.

GEM offers the only open-source and comprehensive global database on midstream oil pipeline infrastructure.

What’s changing elsewhere?

- GOIT now tracks 1,634 oil pipeline projects (some 487,000 km) and 292 natural gas liquid (NGL) pipeline projects (about 111,000 km) worldwide, including roughly 27,800 km of operating crude and products pipelines across the eight countries ringing the Persian Gulf.

- The update finds roughly 32,400 km of oil pipelines in development globally — about 12,300 km under construction and 20,100 km proposed — representing an estimated US$98 billion in capital expenditure.

- The buildout is concentrated in Asia and Africa, which together account for over two-thirds of in-development oil and NGL pipeline km. Asia is building pipelines to feed refineries serving the world's fastest-growing oil demand. Africa is developing this infrastructure to sell newly tapped, stranded crude abroad, though its buildout is overwhelmingly planned rather than explicitly under construction.

Crude oil pipeline construction shifts to Asia and Africa

The four leading subregions by in-development oil and NGL pipeline length are Southern Asia (7,035 km), Eastern Asia (6,490 km), Sub-Saharan Africa (6,031 km), and Latin America (5,693 km). Narrowing in on construction-stage pipelines, India alone accounts for roughly one-third of the global total, at 5,473 km. This includes major projects like the Kandla–Gorakhpur LPG, Paradip–Numaligarh, and New Mundra–Panipat pipelines. By contrast, North America, home to the world's largest operating network, has just 4,400 km in development, and only half of that is under construction, underscoring how new oil pipeline development has shifted decisively toward Asia and Africa.

A buildout for what?

Oil and NGL transmission pipelines are the hidden arteries of the fossil economy, fuelling transport, heating homes, and feeding the world's plastics and fertilizer industries. Yet each new line locks in costs, dependence, and emissions for decades longer than climate commitments say they should taper.

The market backdrop sharpens this question. Last week, the International Energy Agency (IEA) warned that the disruption now reshaping crude flows is set to reverse sharply: As Hormuz reopens and delayed barrels return, the oil market is on course to swing from today's record-low inventories to a surplus of roughly 5 million barrels per day in 2027, one of the largest gluts the agency has ever projected. Much of the planned pipeline buildout, in other words, is being sanctioned into a market that may soon be oversupplied and into prices the IEA expects to fall, deepening the risk that these decades-long assets are obsolete before they ever pay off.

Even as one chokepoint reopens, the world keeps building its dependence on the next one.