Key points

- The energy shocks tied to Iran and the Strait of Hormuz in March 2026 show that even in a relatively balanced liquefied natural gas (LNG) market, disruptions to shipping routes and production can quickly raise delivered prices and tighten access, underscoring the economic and energy-security risks for deeper LNG dependence in regions like Southern Asia.

- Before the conflict, global LNG markets were on a straightforward path to oversupply with new U.S. and Qatari production ramping up through the end of the decade, fueling optimistic demand growth forecasts for Southern Asia. Global Energy Monitor (GEM) finds that LNG terminals and gas pipelines in development in the region total US$107 billion in potential investment.

- However, the major gas importers of Southern Asia — India, Bangladesh, and Pakistan — are likely to encounter barriers to LNG growth even beyond the ongoing conflict, including high fuel costs and high rates of failure among prospective LNG import projects. Over the last ten years, these countries have shelved or cancelled 2–3 times as much proposed LNG import capacity as they have brought online.

- The success or failure of these infrastructure plans will impact the region’s future energy mix. India has the second- and third-largest planned buildouts of LNG terminals and gas pipelines in the world, respectively. Bangladesh and Pakistan have enough proposed LNG import infrastructure to roughly double their existing capacities to import the fuel, and they rank among the top fifteen developers of gas pipelines globally.

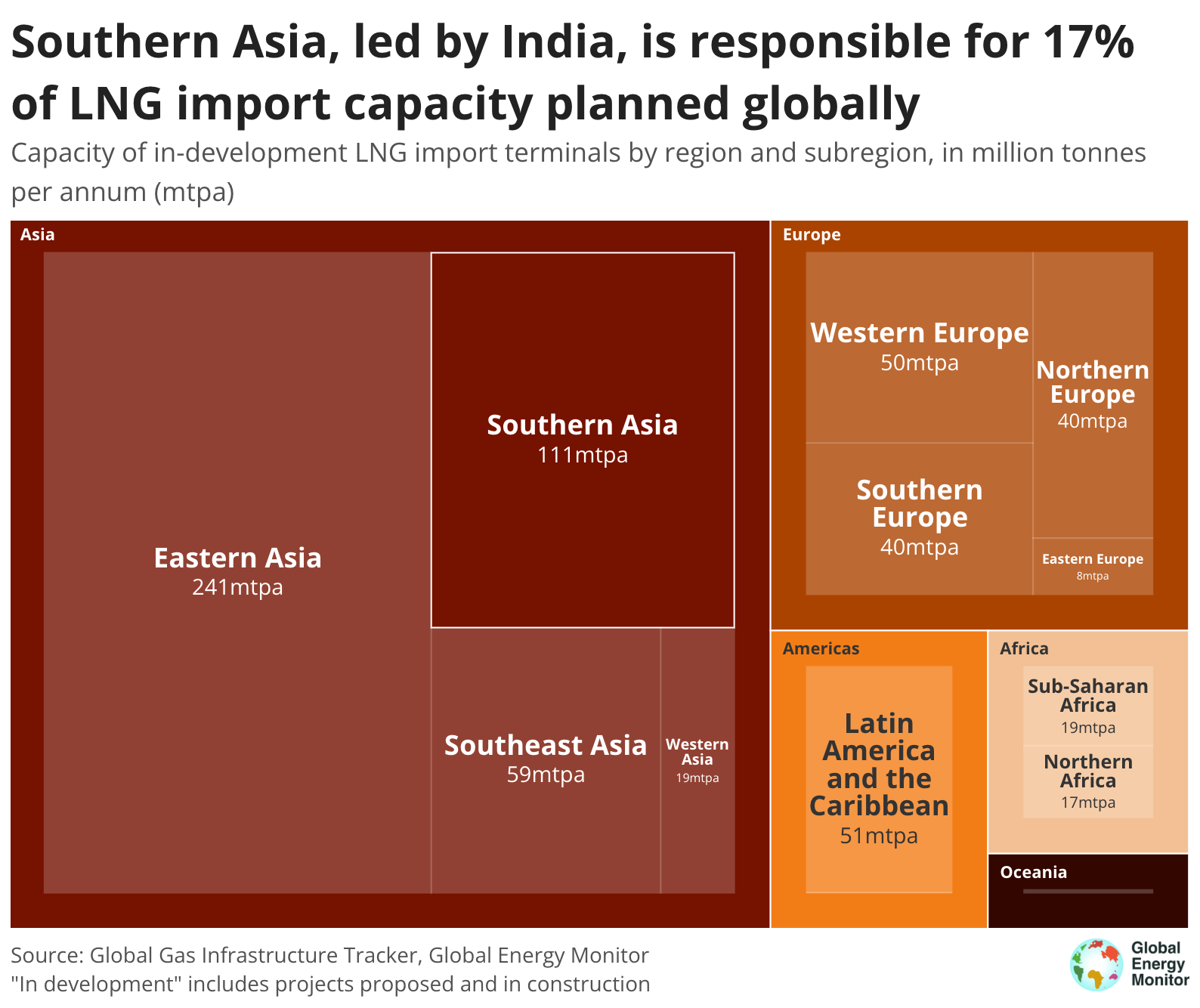

- Southern Asia accounts for 17% of all LNG import capacity in development (110.7 million tonnes per annum) and 17% of all gas pipelines by length (34,146 kilometers), with the bulk of these projects in India.

- Increased dependence on LNG imports is an economic and energy security risk for all three countries, which the governments of Bangladesh and Pakistan have begun to acknowledge through their energy strategies. Renewable power is already outcompeting gas in India and Pakistan’s power sectors, and alternative solutions like green hydrogen can wean the region off of relying on gas imports for industry.

Introduction

The largest economies of Southern Asia — India, Bangladesh, and Pakistan — are price-sensitive gas importers that could, theoretically, be beneficiaries of an incoming glut of liquefied natural gas (LNG). These economies have well-established LNG import industries, growing economies, and declining domestic gas production. According to Global Energy Monitor’s (GEM) Asia Gas Tracker, LNG terminals and gas pipelines in development in the region total US$107 billion in potential investment.

Industry forecasters and the International Energy Agency (IEA) anticipate strong LNG demand growth in regions like Southern Asia. However, whether new LNG demand will materialize to the extent that the industry has promoted is questionable, given the cost of LNG relative to alternatives and a high rate of project failures shown in GEM’s data. Over the last ten years, these countries have shelved or cancelled 2–3 times as much proposed LNG import capacity as they have brought online.

This briefing provides an overview of GEM’s LNG terminal and gas pipeline data in India, Bangladesh, and Pakistan, as well as the challenges these countries face in scaling up this infrastructure, even amid a ramp up in global LNG supply led by the United States and Qatar.

India, Bangladesh, and Pakistan are three of the eight most populous countries in the world, with gas infrastructure plans that could shape their energy mixes for decades to come. India’s gas development is particularly notable from a global perspective; it is the world’s fourth-largest consumer of LNG, and GEM data show it has the second- and third-largest planned buildouts of LNG terminals and gas pipelines, respectively. In Bangladesh and Pakistan, industry plans to build LNG import terminals would roughly double their existing capacities to import the fuel. Southern Asian governments have taken varying approaches to gas’ role in their energy transitions: India is promoting new gas infrastructure and increased consumption, while Pakistan has taken steps toward deemphasizing LNG’s future due to cost, and early indications suggest a new government in Bangladesh may do the same.

For all three of these countries, low spot prices through the end of this decade may make LNG temporarily more attractive, but they also obscure the long-term risks of developing economies reliant on this volatile imported fuel. The short-term risks, too, have surged following the U.S.-Israeli attack on Iran, which threatens to squeeze LNG prices by disrupting shipments through the Strait of Hormuz. Growing deployment of renewable power, energy storage, and other clean technologies can provide a buffer against fluctuating gas markets and serve as a reliable, affordable alternative.

Demand forecasts and infrastructure plans point to LNG growth in Southern Asia

A massive wave of new LNG export capacity led by the United States and Qatar is set to come online over the latter half of this decade. Global LNG export capacity is conservatively set to grow 56% by 2031, counting projects that are already under construction or have reached final investment decisions (FIDs) committing them to construction. Tight LNG market conditions, which peaked in the aftermath of Russia’s invasion of Ukraine, dominated the first half of the decade. Now the LNG market is expected to flip from “famine to feast” with a surplus of LNG supply.

The LNG industry is counting on new supply to lower prices in regions like Southern Asia and drive demand in the power and industrial, as well as others. The world’s biggest LNG trader, Shell, forecasts in its LNG Outlook 2025 that demand for LNG will grow 60% by 2040, attributed in large part to Asia, especially China and India, and the International Group of Liquefied Natural Gas Importers (GIIGNL) finds that Southern and Southeast Asia could have the highest incremental LNG import growth. The IEA, too, bullishly predicts LNG demand growth to grow 60% by 2030 in Pakistan and Bangladesh.

GEM’s infrastructure data confirm there are many Southern Asian gas projects on the drawing board that, if built, would help facilitate this demand growth.

Southern Asia has 110.7 million tonnes per annum (mtpa) of LNG import capacity, or 17% the global total in development (i.e., projects proposed or in construction) as shown in Figure 1. The majority of these projects are based in India, which has 84.6 mtpa in LNG import capacity planned. Bangladesh and Pakistan have proposed 11.3 mtpa and 12.1 mtpa in new LNG import capacity, respectively, enough to roughly double each country’s existing import capacity. Sri Lanka, which is included in Southern Asia in Figure 1, has a single proposed import terminal with a capacity of 2.7 mtpa.

Figure 1

India has the world’s third-largest planned buildout of gas transmission pipelines, after China and Russia, with 19,635 kilometers (km) in development (Figure 2). Almost three-quarters of these pipelines are under construction. Pakistan is developing the tenth-most pipelines by length globally, with 3,893 km in new projects, and Bangladesh is planning 2,695 km. Gas pipelines link LNG import facilities with gas-consuming sectors such as power, industry, and city gas networks. Collectively, Southern Asia is responsible for 17% of all gas pipelines in development.

Figure 2

All three countries are facing declining gas production from mature oil and gas fields. Bangladesh’s gas production fell by 9.3% between 2014 and 2024, and Pakistan’s dropped by 23.6%. While India’s gas production stayed roughly flat over the same period, it is forecast to decline by an average of 3.6% over the next five years.

Despite a wide field of gas projects in development and optimistic demand growth forecasts, Southern Asia’s gas buildout may not materialize as much as expected.

Oversupply: The false promise of affordable LNG

The high cost of LNG in the first half of this decade has curbed Southern Asia’s demand for the fuel. In the summer of 2022, during the gas crisis caused by Russia’s invasion of Ukraine, the Japan Korea Marker (JKM) spot price for LNG went as high as $70 per million British thermal units (mmBtu). Bangladesh and Pakistan endured rolling blackouts because they were shut out of the LNG market at times during the crisis, including when suppliers cancelled contracted LNG in favor of higher-paying European markets. Spot prices have since stabilized (at least prior to the conflict in Iran), with the JKM spot price hovering over $11/mmBtu as of this January. But even at these levels, strong demand growth has yet to materialize in Southern Asia. India’s largest importer, Petronet, said in January that it is still waiting for prices to fall.

With the global supply of LNG increasing by at least half by 2031, the question is whether lower LNG prices will spur demand growth that meets optimistic industry forecasts. Two factors suggest that it will not: infrastructure bottlenecks and the fact that LNG costs may still be uncompetitive with other sources of energy.

Infrastructure bottlenecks could constrain LNG demand growth

For a country to import LNG, it must have sufficient infrastructure to accept, regasify, and transport the fuel to its end use. In aggregate across South and Southeast Asia, there is currently not enough import capacity to realize demand growth forecast by the IEA and others, but projects that are in construction or proposed could close this gap, if built. However, GEM data show that LNG import projects planned in Southern Asia have a relatively high rate of failure; that is, a high share of proposed projects end up shelved or cancelled rather than being brought online. As shown in Figure 3, over the past decade, Southern Asia’s LNG importers have shelved or cancelled 2–3 times as much planned import capacity as they have brought online.

Figure 3

These ratios of project failures to successes are comparable to those of Southeast Asia as well, whose emerging economies could account for much of the world’s LNG demand alongside Southern Asia and China. It is noteworthy that these rates of project failures are relatively high compared to Europe, the other major LNG importing region, and not necessarily characteristic of the LNG industry globally. In Europe, there is a roughly even ratio of LNG import projects that were failed vs. built, shown in Figure 4.

Figure 4

Project failures are likely to bottleneck gas development in Bangladesh and Pakistan, according to work by energy analyst Seb Kennedy in coordination with GEM. Projects are more likely to fail in Southern and Southeast Asia for diverse reasons including political turmoil, slow contract negotiations, a lack of distribution infrastructure (specifically pipelines), and lawsuits, among others.

As recent examples, in October 2024, Bangladesh’s interim government scrapped deals with contractors developing Summit Matarbari FSRU and Payra FSRU, and these projects have yet to definitively move forward. In Pakistan, Pakistan State Oil LNG Terminal, LNG Easy Floating LNG Terminal, Daewoo Gas LNG Terminal were all inferred shelved by GEM in 2024 or 2025, meaning that GEM has marked them inactive due to no demonstrated progress in over two years.

Insufficient LNG import capacity is unlikely to bottleneck India’s gas development because it has so much existing import infrastructure, which has been operating at low utilization rates, alongside plans to build 84.6 mtpa in new capacity. Of four LNG import projects that came online in Southern Asia over the past five years, all are located in India. A lack of gas pipelines has been a bottleneck for Indian gas development, although pipelines currently under construction are expected to better connect the country.

In its Gas Outlook 2025, the IEA acknowledges the constraints posed by the region’s LNG infrastructure: “If existing infrastructure in Southeast Asia and other emerging LNG-importing regions is not expanded, about one-quarter of the demand response may be at risk of not materializing.”

Cheaper LNG may still be uncompetitive

LNG that is relatively cheap during a period of oversupply may still not be competitive with alternatives. As the IEA writes in its World Energy Outlook 2024, “Gas-importing emerging and developing economies would generally need prices at around $3-5/mmBtu to make gas attractive as a large-scale alternative to renewables and coal, but delivered costs for most new export projects need to average around $8/mmBtu to cover their investments and operation.” According to the Institute for Energy Economics and Financial Analysis (IEEFA), these “breakeven production costs should serve as a long-term anchor for prices,” even if spot prices temporarily dip below them.

Meanwhile, renewable power costs are falling globally and across Southern Asia, leading to rapid expansions of solar power in Pakistan and India. And of the industrial sector broadly across Asia, IEEFA writes, “With domestic gas production declining in many countries, introducing more expensive gas from harder-to-produce domestic resources or LNG imports could harm the competitiveness of local industries established on legacy, low-cost gas sources.” Bangladesh's industrial slowdown, for example, has been attributed at least in part to the high cost of LNG imports.

There are logical inconsistencies between maintaining LNG prices that are both suitable for strong growth among price-sensitive Asian importers and the bottom line of producers in the United States and elsewhere. Shell’s LNG Outlook, which suggests LNG demand will grow 60% by 2040, would require new supply beyond the current wave of new export projects, but prices low enough to stimulate high demand in Asian economies are unlikely to justify new investments in export infrastructure. As Reuters columnist Clyde Russell writes, “In the coming decades LNG companies likely have a choice between higher volumes or higher prices, but can't have both.”

Importantly, the period of oversupply is likely to only last a few years. While importers may temporarily buy spot LNG at a discount and lock in better long-term contract terms for a period, market conditions will eventually stabilize and again become less favorable for importers. The Oxford Institute for Energy Studies expects LNG markets to rebalance in the early 2030s, and Qatar Energy has argued that, in an LNG-fueled AI boom, the period of oversupply could end by 2030.

For now, though, the straightforward path to oversupply has been called into question by the conflict in Iran and impacts on global LNG markets. One-fifth of the world’s LNG passes from Qatar through the Strait of Hormuz, over 80% of which goes to Asian buyers. Qatar’s massive Ras Laffan LNG complex was shut down on March 2 due to a drone attack, and shipping activity through the strait has ground to a halt. It remains to be seen how long Qatari LNG production and shipping will be disrupted, but the crisis highlights that favorable market conditions for LNG buyers are neither predictable nor inevitable.

Southern Asia’s governments plan diverging futures for LNG

There is evidence that LNG has been uncompetitive in India, Bangladesh, and Pakistan, though Southern Asia’s governments have adapted differently to this economic reality. India is promoting LNG and gas development, Pakistan announced plans to shift away from LNG after the global gas crisis earlier this decade, and Bangladesh’s new government is likely to promote renewables and domestic gas over fuel imports.

India

As energy demand in India continues to grow rapidly, the government has set a goal of increasing gas consumption threefold, bringing it to 15% of the country’s energy mix. The government’s National Gas Grid project is intended to connect the country’s major gas supply and demand centers, and the 14,517 km of pipelines currently under construction will bring the country closer toward that goal. A lack of pipeline infrastructure has been a bottleneck for gas demand growth in India, along with costs and regulatory and policy factors. India’s government has been supportive of new LNG terminals and recently greenlit a 19.92 mtpa expansion at Hazira LNG Terminal, the largest single import project currently planned in the world.

In contrast to Pakistan, Bangladesh, and much of Asia, India’s power sector accounts for a relatively small share of its gas use, just 13% last year, and just 3% of India’s electricity generation came from gas. Gas use is cost prohibitive in the power sector compared to coal and renewable power — which now accounts for 40% of installed capacity in India. Several operating and planned gas-based power plants were forced to shut down or were cancelled over the last few years due to the high cost and low availability of gas. The IEA still forecasts some demand growth in the power sector but states that city gas distribution and industries such as iron and steel and refining could be the main drivers of new demand.

India’s fertilizer industry is the single largest-consuming sector of gas, accounting for 29% of its consumption last year, although the IEA notes that demand growth may be limited as “no new gas-based capacity additions are foreseen.” Fertilizer production has already been impacted by the reduction of Qatari LNG supplies due to the conflict in Iran. “If the war continues, it will be a matter of concern for us,” said an industry representative.

Even with more pipeline infrastructure in place, there are reasons to doubt that much of India’s growing energy demand will be met by LNG as the IEA and others might expect. An IEEFA analysis found that LNG has only been competitive in India’s highly-subsidized fertilizer industry and that alternatives like renewable power, coal, and domestically produced gas are more likely to be adopted in sectors such as power generation, steel production, and city gas distribution. It is for this reason and others, like India’s pipeline bottlenecks, that of India’s eight operational LNG import terminals, six operated at utilization rates below 50% in fiscal year 2025. If LNG prices remain elevated due to the conflict in Iran, or other unforeseen supply disruptions, there is a heightened risk that new LNG terminals and pipelines could be stranded assets due to underutilization.

The CEO of the top Indian LNG importing company, Petronet, said prices for LNG would need to be between $6 and $7/mmBtu for consumption in India to increase significantly, but as the LNG analyst Justin Mikulka writes, this price point may be untenable for U.S. LNG exporters.

India had the third-largest renewable power generation in 2024, and the country is on track to meet 42% of its electricity demand with renewables by 2030, according to Ember. Strong growth in renewables will likely continue to edge out gas’ minimal role in the power sector. While renewables can eventually replace gas as an energy source for the industrial sector, alternative solutions like green hydrogen for the fertilizer industry, via electrolysis or biomass gasification, can provide clean, domestically sourced energy while further reducing the need to import expensive LNG.

Bangladesh

In February 2026, Bangladesh elected a new government, the Bangladesh Nationalist Party (BNP), which has signaled it may seek to shift the country away from imported fuels like LNG. In an election manifesto, the BNP said it would aim to boost renewable energy from a 4–5% share of Bangladesh’s power mix to 20% by 2030, and that it would advance the country’s domestic gas production by developing offshore blocks and strengthening partnerships with foreign firms. Whether these commitments will be put into policy will become clearer over time.

Prior to this government, Bangladesh had appeared to be betting on LNG to meet its energy needs. A draft energy master plan published in January, covering 2026–2050 in three phases, mostly prioritized offshore exploration, increased gas extraction, and LNG supply security in its first stage, ignoring Bangladesh’s energy transition goals. In 2025, Bangladesh imported 109 LNG cargoes, and Bangladesh has been notable in the region for the degree to which it has committed to new long-term contracts, with three beginning in 2026. Bangladesh still has 11.3 mtpa of LNG import capacity in development, which would more than double its existing 8.3 mtpa, although a failure to expand this infrastructure would likely bottleneck LNG development in the country. A lack of pipeline connectivity is also a significant impediment to getting new gas to market in Bangladesh and motivated a push to expand the pipeline network. There are 2,695 km of pipeline in development in Bangladesh, but just 8% of that is under construction.

Petrobangla, the national oil and gas exploration company, warns that “fluctuating LNG prices could further strain the country’s finances.” According to Petrobangla, the cost of LNG exceeds the cost of domestic gas by a factor of nearly twenty. These high fuel costs are causing factories to decrease production, lowering the country’s economic growth. The Business Standard has estimated that Bangladesh’s foreign currency obligations from the energy and power sectors to be US$20 billion per year, and that these obligations could rise up to US$24 billion more if the country’s energy needs are met by imported LNG and oil.

With a renewable energy penetration of less than 2%, Bangladesh ranks in the bottom 10% of countries by share of renewables generation. If Bangladesh were instead to put this momentum and investment into solar power and energy storage, the country could more cheaply and quickly achieve its energy ambitions.

Pakistan

In 2023, Pakistan’s government reversed course on its strategy to increase imports of LNG and other fuels in response to the economic impacts of the global gas crisis set off by Russia’s invasion of Ukraine. According to the energy ministry, the country would stop building new power plants relying on LNG or other imports, and focus on domestic power capacity from renewable, nuclear, and locally-mined coal power. As of 2025, Pakistan’s Minister of Petroleum clarified that the policy change “is not a temporary blip” and that the government did not see a place for new LNG plans despite there being projects in development.

However, this move away from LNG is not a move away from gas. Pakistan’s Minister of Petroleum was clear that the country would “incentivize local gas exploration to help reduce costs for power producers and cut back debt.” By December 2025, the Pakistani government was already following through on those plans when Pakistan's state-run Oil & Gas Development Company (OGDC) announced plans for a major expansion of unconventional gas developments starting in early 2026, “aiming to boost production and reduce reliance on imported liquefied natural gas.”

Because these new discoveries and the areas targeted for further exploration largely contain unconventional tight gas resources requiring specialized drilling or occur in deep water, it will likely take longer to bring those resources to market; GEM finds that, on average, oil and gas fields now take about fifteen years from discovery to production.

Meanwhile, solar power has already proven a cheap and rapidly deployable solution in Pakistan. Solar power’s share in generation has more than tripled in three years, to 14% of generation in 2024, driven by homes and businesses installing rooftop solar in response to expensive and unreliable electricity from the grid. Solar deployment has been a contributing factor to low gas demand and the country delaying LNG shipments.

Conclusion

As spot prices for LNG fall over the coming years, importers in Southern Asia and producers seeking to supply the region risk being misled by a mirage. The price of LNG is volatile and expensive enough that it is unlikely to be competitive in the long run against alternatives, potentially weighing down the growth of emerging economies that build around it. LNG producers risk overestimating demand growth through optimistic forecasts like the Shell LNG Outlook, without factoring in potential chokepoints. Price-sensitive Asian economies and producers are unlikely to find prices that facilitate such high growth. And as shown in GEM data, proposed LNG import terminals in Southern and Southeast Asia have high rates of failure, and could limit the regions’ capacity to import the fuel.

In the immediate term, the fallout from the U.S.-Israeli attack on Iran has highlighted the fragile assumption that LNG imports will be affordable and reliably delivered to Asia, as prices are squeezed by the disruption of Qatari LNG shipments through the Strait of Hormuz. “The pricing implications are savage,” writes Seb Kennedy, with futures for the JKM spot price jumping 40% as of early March. Because Qatari LNG shipped through the Strait of Hormuz is overwhelmingly sold to Asian buyers, the region is particularly exposed. Industry officials in Bangladesh and Pakistan compared the current situation to the energy crisis following Russia’s invasion of Ukraine.

There are myriad other complicating factors to bullish demand growth narratives in South and Southeast Asia, writes Naish Gawen of Data Desk. The ongoing shortage of gas turbines could keep new power plants from moving forward with construction (globally, GEM has found that two-thirds of gas power projects in development have not announced a turbine manufacturer). LNG is increasingly sold on the spot market or through destination-flexible contracts to traders like Shell, rather than end users like Asian utilities, calling into question whether this LNG will actually find buyers. Additionally, LNG terminals take several years to build even without significant delays — on average 4–5 years in Southern and Southeast Asia, according to GEM project timeline data. Finally, renewables deployment is accelerating in the region and competing with gas demand growth.

The costs of renewable power have been rapidly falling, and, for the power sector, offer a secure and competitive alternative; the International Renewable Energy Agency (IRENA) found that, globally, 91% of new utility-scale renewable power outcompeted fossil fuel alternatives. Likewise, energy storage solutions are improving, making inroads in Asia, and can offer grid flexibility eroding gas’ assumed role in peaking and balancing. Reducing the consumption of gas and other fossil fuels from the industrial sector in India and elsewhere is a technical and policy challenge. But it is one that is incentivized by countries’ own decarbonization targets, trade policies favoring low-carbon goods, and energy security through reduced reliance on fuel imports, and it is achievable through technical solutions such as electrification, energy efficiency, and green hydrogen via electrolysis or biomass gasification.

Even in oversupply, beyond the current energy shock, Southern Asian importers of LNG should remain clear eyed about its limitations. Growing deployment of renewable power and other clean technologies offers a foundation for more sustainable and competitive economies.