Pedal to the Metal is an annual survey of the current and developing global iron and steel plant fleet. The report examines the status of the iron and steel sector compared to global decarbonization roadmaps and corporate and country-level net-zero pledges.

This year’s analysis draws from GEM’s Global Iron and Steel Tracker (GIST) and the Global Iron Ore Mines Tracker (GIOMT). Together, these tools provide detailed, asset-level data on 1,293 iron and steel plants in 91 countries and nearly 700 operating and proposed mines worldwide.

The 2030 deadline: A closing window for transition

With 2030 decarbonization deadlines approaching, the global iron and steel industry is running out of time to shift away from coal-based production methods. Continued investment in coal-based capacity and underinvestment in green hydrogen threaten net-zero targets.

Now more than ever, it is crucial to disrupt emissions-intensive blast furnace developments and redirect resources to iron and steelmaking technologies that align with net-zero goals.

While gains in Electric Arc Furnace (EAF) capacity and surge in green direct reduced iron (DRI) announcements are encouraging, these advances remain overshadowed by blast furnace expansion, fossil-based DRI growth, and reinvestment in legacy coal assets.

Incremental progress in cleaner technology

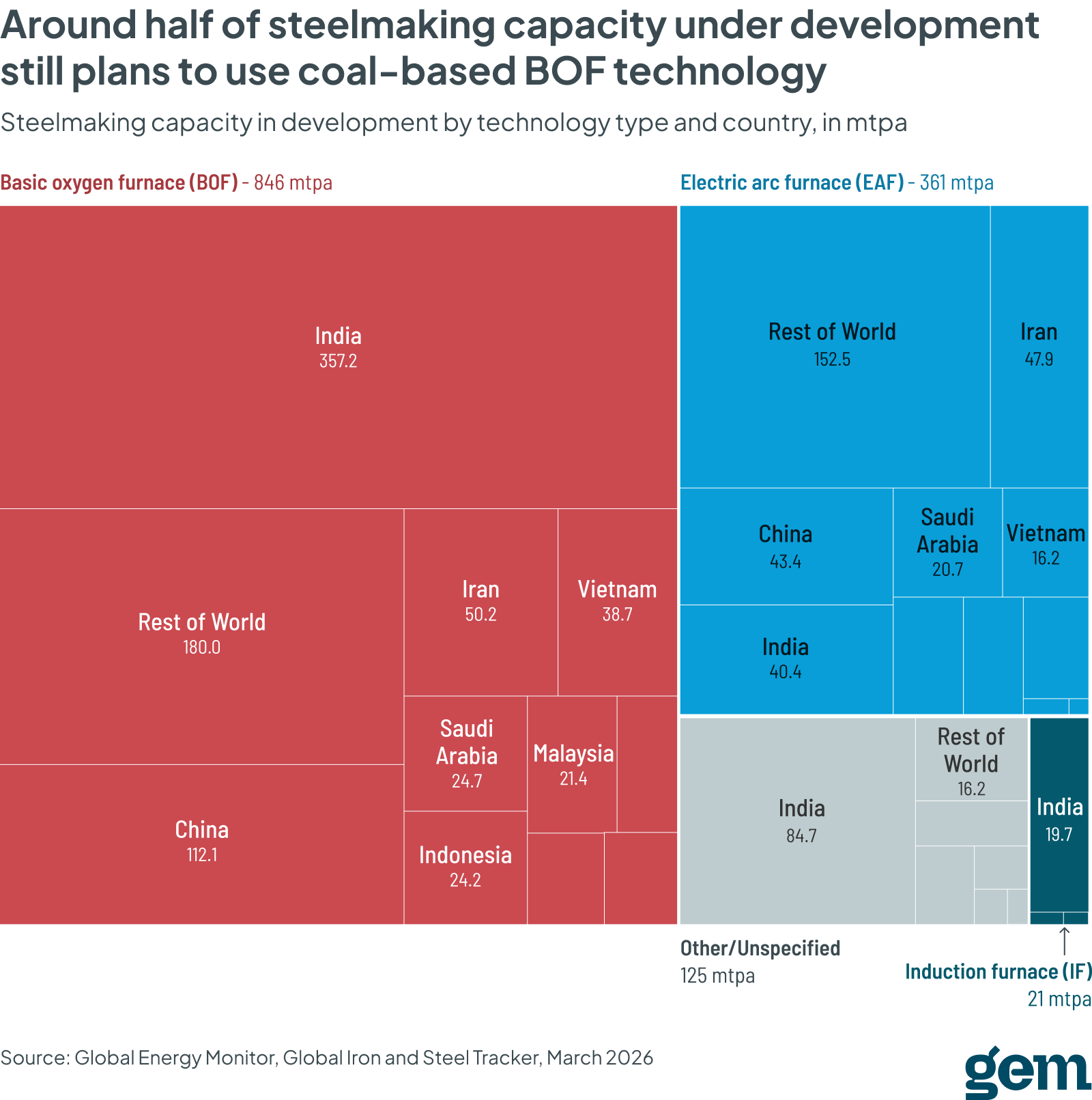

Global steel decarbonization is slowly progressing, with EAF capacity increasing its share of global operating capacity by 1% in the past year to 34%. Currently, EAF represents 50% of developing steel capacity and 71% of projects that have already broken ground.

However, the green hydrogen challenge remains a critical bottleneck. While green H2-based DRI is key to the sector’s decarbonization plan, just 2% (4 mtpa) of operating DRI capacity uses green hydrogen as a primary reductant. While 19% of planned capacity intends to use hydrogen upon startup, these plans will not become a reality without a major shift in the available reductants and infrastructure.

India and China: The primary drivers of change

The industry's transition rests heavily on the choices of two nations, which together plan 86% of all new coal-based capacity globally.

The outlook remains bleak for steel’s transition away from fossil fuels. The ball is in India and China’s court, as the two countries plan 86% of new coal-based capacity. Pivoting to lower-emissions technologies and using existing EAF capacity more effectively are two immediate steps the countries can take to have a profound effect on the direction of the steel industry.

Astrid Grigsby-Schulte, Project Manager of the Global Iron and Steel Tracker at GEM

India has surpassed China as the primary driver of global steelmaking development, accounting for 42% (357 mtpa) of all developing capacity. This expansion is heavily reliant on coal-based technology, with India now responsible for nearly two-thirds (62%) of all BOF capacity in development globally. However, because just 5% of India's developing ironmaking capacity has actually broken ground, a significant intervention opportunity remains to redirect the country toward decarbonized routes.

China remains the global leader in operating capacity, but its growth appears to be leveling off. While 39% of developing capacity in China will rely on EAF technology, the impact of this shift is constrained by vast coal-based legacy assets. Approximately 94% of China's massive blast furnace capacity has no retirement plan, and the country remains the second-largest net developer of BF capacity after India.

Doubling down on coal: The lock-in crisis

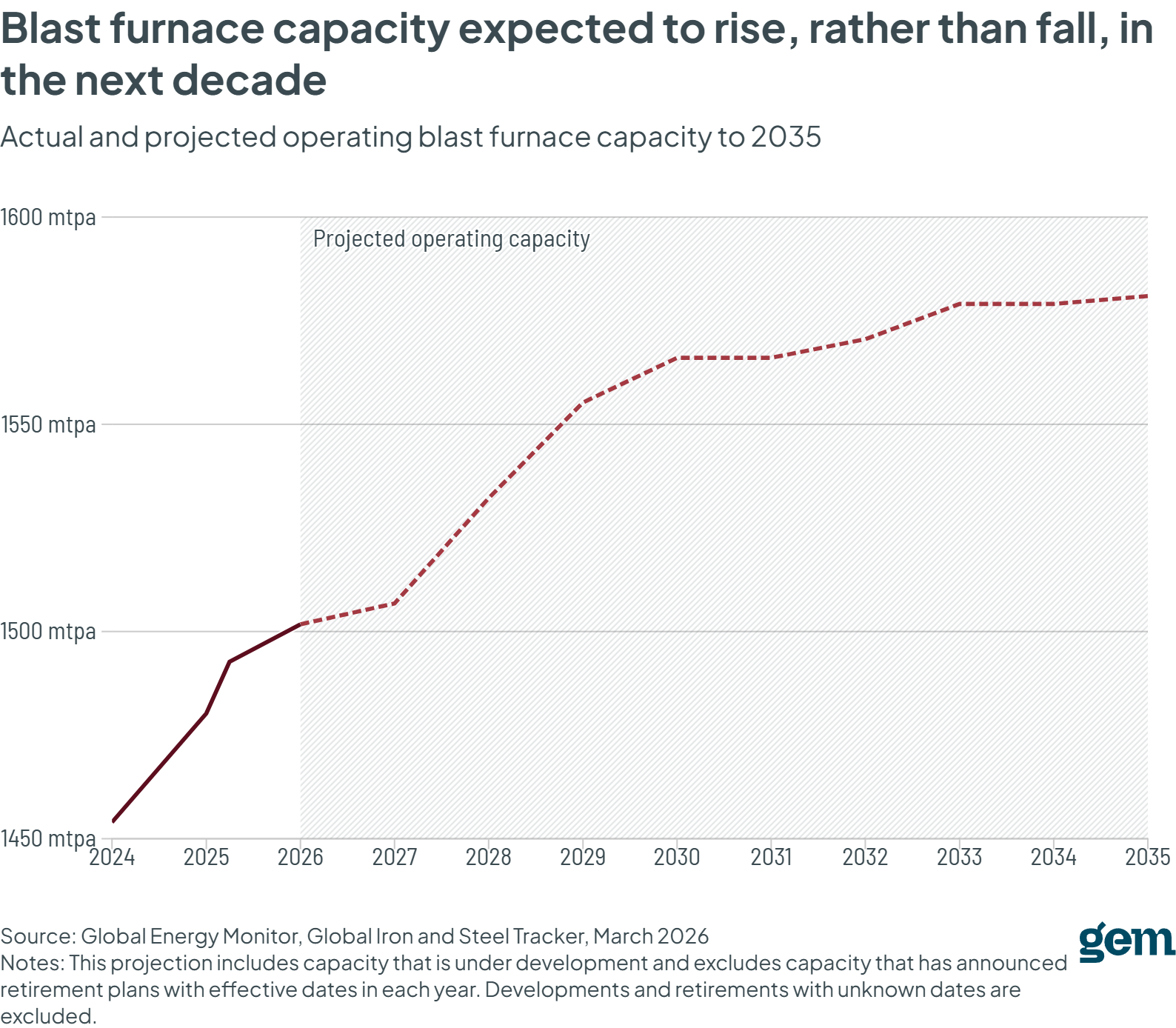

The persistence of coal-based steelmaking puts decarbonization at risk. There is currently 319 mtpa of blast furnace (BF) capacity under development — a 5% increase over last year. While 141 mtpa of currently operating BF capacity has announced retirement plans, new investments are expected to result in a net gain of 178 mtpa of BF capacity if all plans proceed.

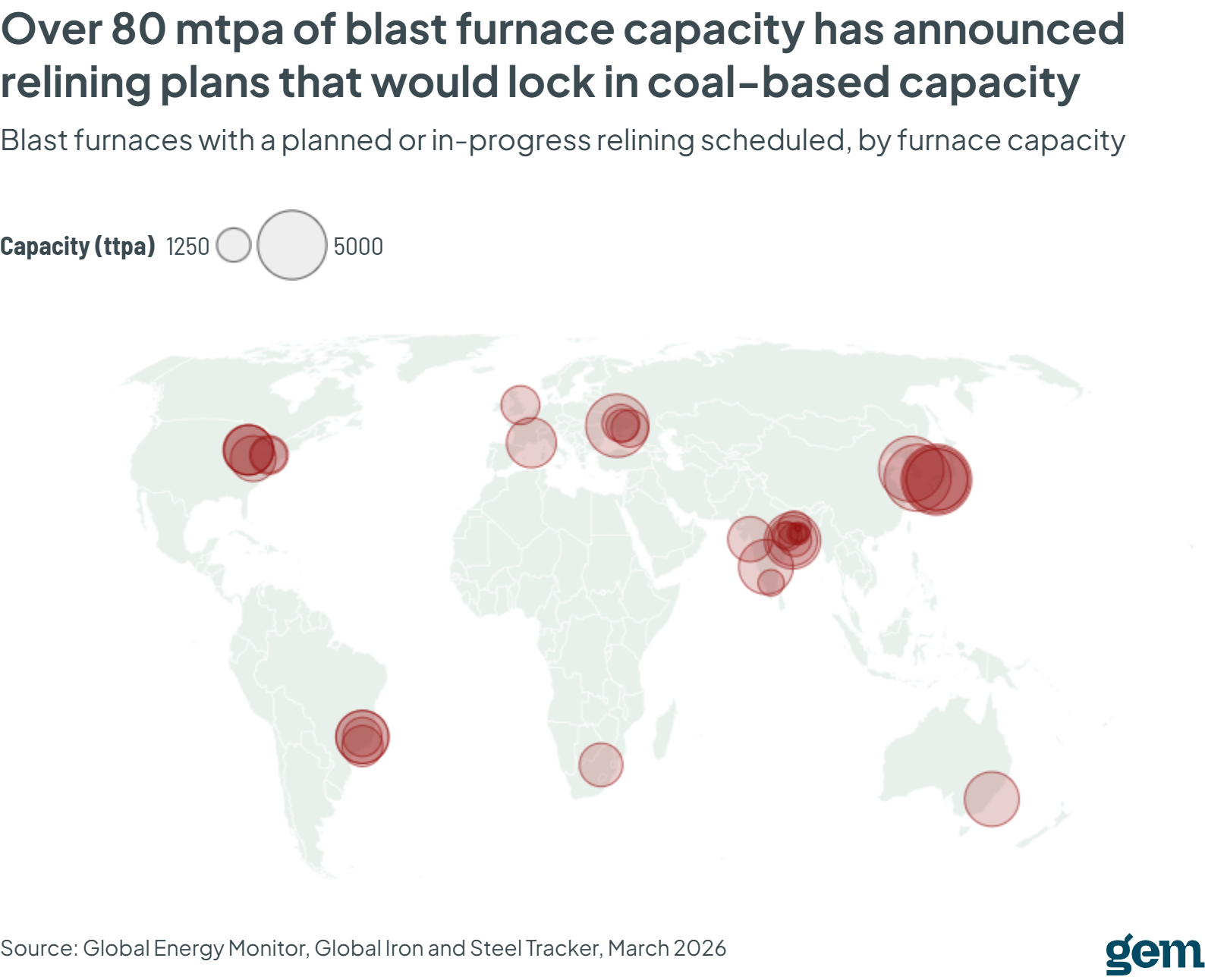

A critical "lock-in" signal is the 80 mtpa of existing BF capacity currently planning or undergoing relining. With an average global campaign of 15–20 years, these relining events signal an intention to operate coal-based units long-term, locking in carbon emissions and diverting capital from green technologies.

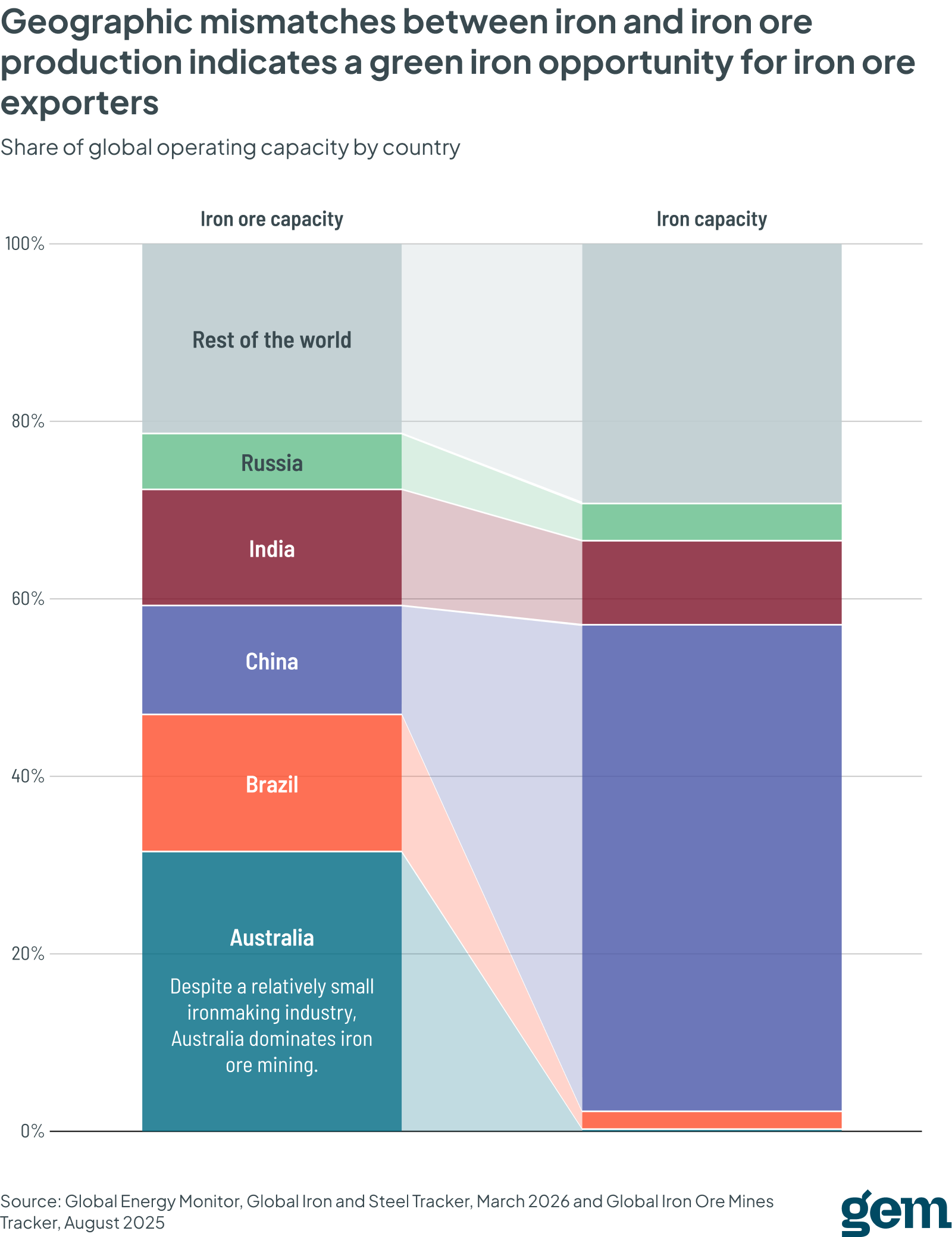

Upstream supply chains and regional shifts

The pivot toward DRI-based ironmaking heightens a supply-side constraint: DRI requires high-grade ore (over 67% iron content), which represents only about 4% of the global iron ore supply.

Major exporters like Australia and Brazil dominate iron ore mining but consume less than 10% of what they mine, presenting a green iron opportunity to develop DRI infrastructure locally.

A critical decade for intervention

The next ten years represent a vital window for the iron and steel industry. With the industry responsible for 11% of global CO2 emissions, the decisions made today regarding relining and new buildouts will determine the emissions profile for the next two decades.

To meet global climate goals, the steel sector must move beyond incremental gains. This requires a rapid scale-up of green hydrogen infrastructure, a re-evaluation of coal-based projects that have not yet broken ground — particularly in India — and a more effective utilization of existing lower-emissions capacity. Without these structural shifts, the industry risks entrenching a "coal lock-in" that will make the net-zero transition impossible.