Key points

- It now takes an oil and gas field three times as long to come online compared to the period 1960–1980, when the majority of the world's top producing fields were discovered, an increase of over ten years.

- New projects face additional challenges, such as increased technical and regulatory complexity, sub-optimum reservoir characteristics, heightened ecological impacts, lower investor confidence, higher costs, and infrastructure scarcity.

- The average fifteen year lead time showcases the risks associated with new, costly projects that can become stranded assets under climate uncertainty.

- The remaining stock of new oil and gas projects is harder, and often more dangerous, to develop, making investment in a decarbonized future a safer bet.

Introduction

Developing a new oil and gas field takes 3.1 times as long as it used to. Analysis of the Global Oil and Gas Extraction Tracker (GOGET) shows that 2025 startups of new conventional fields took over fifteen years to come online from discovery, following a trend of increasing development timelines. New projects are more complex in myriad ways — geologically, ecologically, economically, politically, and often a combination thereof. According to the International Energy Agency (IEA), easier and more accessible fields have been “thoroughly mapped and developed, leaving primarily smaller, deeper and more technically challenging fields.” This complexity has led to the increase in time from when a discovery is announced to the first hydrocarbons being sold to market. Longer lead times have implications for project uncertainty and phaseout strategies, as decisions made today are betting on an unknown future and risk locking in production for future decades.

Long term trends in startup times

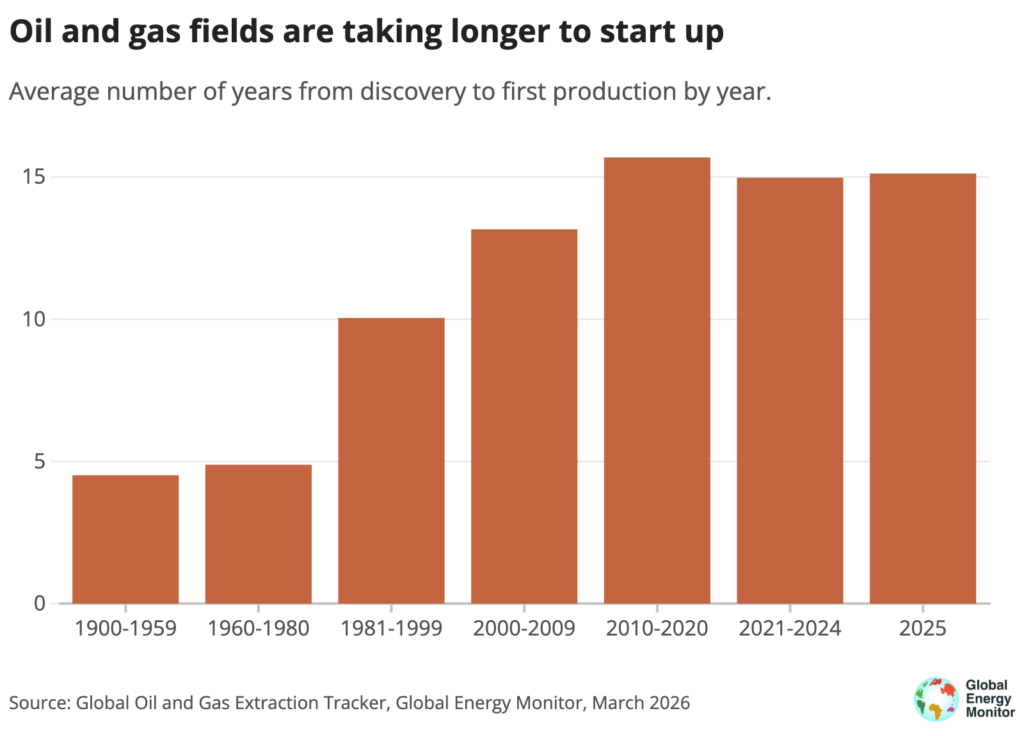

The period between 1960–1980 is considered the peak of oil and gas discovery and exploration. Many of today’s biggest producers were discovered and came online in those 20 years. According to GOGET, from 1960–1980, fields began production an average of 4.9 years after discovery. Between 2000–2009, they took thirteen years for the same process. Between 2010–2020, they took nearly sixteen years, and in the first half of the 2020s, the average was fifteen years. The trend holds true for 2025, when fields averaged 15.1 years.1

Figure 1

Fields that started up between 2010–2020 took the longest, on average, from discovery. The year 2019 shows the highest average lead time of 20.7 years. Six of these projects were in Russia, including the Chayandinskoye, which was brought online 36 years after discovery, requiring a massive pipeline project to connect it to the market. Some strategic shifts have brought lead times slightly lower than the 2010–2020 timeframe, but the past five years remain significantly higher than the late 1900s and early 2000s.

These trends hold across oil, gas, and combined fields — all fuel types take longer to start up now than in previous decades. Across the entire dataset, offshore fields take around three years longer in lead time than onshore fields. Oil fields started up one year quicker than gas fields and three years quicker than combined projects.

This analysis of GOGET is directionally aligned with previous analyses, including one the IEA published late last year finding the “overall development timeline for new projects has risen over time” with the time from discovery to final investment decision (FID) to production growing in recent decades.2

Legal and regulatory challenges, reservoir composition, and a pandemic slowed development and increased costs for 2025 startups. Equinor’s Johan Castberg oil field was initially expected to come online in 2022, then in 2024, before ultimating beginning production in March 2025. Among the quickest turnarounds of 2025 startups was EOG Resources Trinidad 50/50 Mento project with BP Trinidad and Tobago (BPTT) which took five years from discovery to first production. The longest was Libya’s Chadar field — the “long-stalled” project was discovered in 1968 and brought into production last year.

Figure 2

Prior development times

Between 1960–1980, GOGET data show oil and gas fields took an average 4.9 years of lead time from discovery to startup. Quick turnarounds were common then, even for giant fields. Cantarell, one of the world’s largest conventional oil projects, started up in 1979, three years after its discovery. At its peak, the Mexican field produced 2.14 million barrels per day in 2004, about 3% of global production. Similarly, Hassi R'Mel in Algeria was discovered in 1956 and started production five years later 1961. These reservoirs are massive but relatively simple geologically and developmentally when compared to the newest projects coming online.

Reasons projects are taking longer to develop

Technical complexity

Recent oil and gas field startups are more technically complex than previous projects. Easily accessible, conventional onshore fields were developed early, and the fields left are more difficult to bring online.

As an example, the “20K technology” fields in the U.S. Gulf of Mexico (GOM) target ultra-high pressure, previously inaccessible, hydrocarbon reserves as shallower fields mature. 20K projects target reservoirs that were discovered years ago but were originally deemed “off-limits” due to extreme pressure and the necessity for new technical innovations to handle it. Previous technologies were capped at 15K pounds per square inch (psi) of pressure. In addition to the novel technology needed, the target area has challenges due to its reservoir quality and makeup.

Beacon-operated Shenandoah field started up in 2025. Shenandoah was initially discovered in 2009, but was delayed in development until after Chevron’s Anchor field came online in 2024. Anchor opened up a “new chapter” as the first 20K project in the GOM. New fields utilizing this technology include Kaskida and Tiber, aiming to come online 23 and 20 years after discovery, respectively.

Technically complex projects face additional risks due to their extreme pressure and temperatures, according to the U.S. Bureau of Ocean Energy Management. With increased likelihood of blowouts, these fields were “previously deemed too risky,” and opponents claim they may result in spills and are an “unacceptable threat” to the local ecosystem.

Pavel Sorokin, an executive in Russia’s Minister of Energy, has said that by 2030, 80% of the country’s production could come from “hard-to-recover" reserves, up from 32% in 2025. That term includes unconventional production but also high-pressure and ultra-deepwater fields, remote locations, as well as sour gas reservoirs — reserves that are high in concentrations of hydrogen sulfide (H2S). The government has supported shifting towards these reserves and increasing their role to maintain Russia’s position in global markets. The Salmanovskoye field, discovered in 1979 and started up in 2023, illustrates this position in practice. The field was developed in the “remote and inaccessible” Gydan Peninsula as a part of Arctic LNG-2. Oil and gas extraction in the harsh Arctic conditions requires specialized equipment and infrastructure and is considered one of the costliest ventures in the industry.

The IEA lists complex deepwater projects with additional safety concerns as a reason for longer project timelines. With the prominence of offshore fields rising, construction timelines are elongating to accommodate more advanced engineering.

Reservoir composition

The composition of reservoirs impacts development timeline and planning. Sour gas reservoirs have higher concentrations of hydrogen sulfide than sweet gas. The concentration of this toxic gas leads to challenges with equipment and risks to human health. Historically, “it was considered difficult and uneconomic to pursue developmental projects for sour gas,” but in order to start up new projects, companies are turning to sour gas. For example, in Malaysia, developing the Lang Lebah is considered the key to unlocking other new fields with high levels of CO2 and hydrogen sulfide in East Malaysia. Lang Lebah was discovered in 2019 and was anticipated to have a relatively rapid development, as PTTEP targeted FID in 2024. However, as of 2025, it faced an “uncertain future.”

The Barossa gas field started up 19 years after its discovery. The field reportedly has the highest proportion of reservoir CO2 in Australia, leading the Environment Centre NT, to call it Australia’s “dirtiest gas field,” with the group accusing the project promoters of “literally scraping the bottom of the barrel” by extracting from it.

Ecological impacts

Pressure and composition have led to longer lead times, while other fields are risky due to their proximity to protected areas. A recent analysis by the Environmental Investigative Forum (EIF) revealed that active exploration and production licenses are located in more than 7,000 protected areas across 99 countries. About half of these protected areas, which include IUCN, Ramsar, and UNESCO sites, among others, are entirely covered by hydrocarbon licenses.

The cross-border Greater Tortue Ahmeyim Project (GTA) consists of two fields, Tortue in Mauritania and Ahmeyim in Senegal. Tortue was discovered in 2015 and Ahmeyim in 2016. In 2018, when FID was announced, the project was scheduled for 2022 first gas. GTA raises the risk of biodiversity loss due to its proximity to the world's largest cold-water reef, national parks, and marine protected areas. In early 2025, about ten years after discovery and three years behind schedule, first gas flowed from GTA.

The Lake Albert project in Uganda includes the Tilenga and Kingfisher fields and marks the start of the East African Crude Oil Pipeline (EACOP) stretching from Uganda to a port in Tanzania. The project reached FID in 2022. TotalEnergies’s Tilenga and CNOOC’s Kingfisher are expected to start producing in 2026, 20 years after discovery. The project has encountered years of delays amid criticism from civil society and local communities. In addition to the negative impact on local communities and threats to the freshwater resource of Lake Albert, Tilenga’s partial location inside the Murchison Falls National Park has raised additional criticism about habitat destruction and impacts on biodiversity and tourism within a legally protected area.

To read more about the ecological risks of deepwater drilling see last year’s GOGET briefing.

Regulations

Regulatory bodies around the world have varying requirements governing extraction, and in some countries those are becoming more stringent.

The United Kingdom, for example, released new guidance in 2025 calling for environmental impact assessments to now cover scope three emission, defined as “all indirect emissions that occur in the value chain,” most of which come from the combustion of fuels. Rosebank oil field was discovered in 2004, and FID was taken in 2023, targeting a “2026–2027” startup. Rosebank is now up for approval under the new guidance, after its previous approval was ruled unlawful.

New stringent environmental and safety regulations may extend permitting periods. As rules become tighter and more comprehensive, companies are forced to spend additional time and money navigating these systems.

Capital discipline, portfolio prioritization, and global market conditions

Publicly traded international oil companies exist to maximize profits and shareholder value. Sometimes, the most economical move is to hold development of a field until a higher price will be paid for the oil and gas or a cheaper way to develop is identified. Oftentimes, this manifests as companies waiting until a project can be developed as a complex, sharing infrastructure such as gathering pipelines and production hubs.

One example is tiebacks, which connect new fields to existing production infrastructure via undersea platforms. According to Chevron, tiebacks “add shareholder value by lowering development costs.” The West Barracouta field was discovered back in 1969 but did not start production until 2021 when it was developed as a tieback.

The age and status of existing infrastructure may also be a factor in investment decisions, as any retrofits impact development costs, as shown by the example of Venezuela. After the U.S. removed Venezuelan President Nicholas Maduro from power and the country in early January 2026, President Trump held a conference with CEOs of oil and gas companies. ExxonMobil’s Darren Woods called the country “uninvestable,” as some speculated over how Venezuela's high breakeven costs make it uneconomic.

Overall, trends are pointing toward waning investor confidence in risky projects. But companies' capital discipline has not been perfect. According to an Australasian Centre for Corporate Responsibility (ACCR) analysis, projects are routinely late and over budget. In fact, ACCR concluded an analysis of ten companies stating that “ceasing conventional upstream exploration and development is more valuable than continuing it.”

A closer look at Venezuela

U.S. plans to exploit Venezuelan oil reserves are in line with the overall trend discussed here of more complicated projects being taken on to extract new resources. Reviving the Venezuelan oil and gas industry is expected to cost between US$80 and $183 billion. According to analysts, there are economic, geologic, and engineering challenges to boosting production in the country from existing and new fields. Given the geopolitical implications of any new production, the fifteen year startup from discovery is potentially an underestimate for any new fields discovered there.

In-development projects in the country have already faced substantial delays to startup. The Manakin-Cocuina complex, Dragon field, and Loran-Manatee complex were all discovered in the early 1980s but have not yet extracted hydrocarbons.

The heavy crude in Venezuela is considered the dirtiest type of oil, producing as much as four times the greenhouse gases as conventional oil. As the industry moves to more risky production, companies are still hesitant to bite on new, expensive, ecologically and environmentally risky oil from Venezuela.

Infrastructure and market access requirements

Sharing infrastructure can bring down costs for oil and gas developments, so it stands to reason that building entirely new infrastructure in frontier basins is a complicated, costly, and slow process. The 2024 GOGET briefing found that significant discoveries were made in regions with little to no historical production — Guyana, Cyprus, and Namibia. While Guyana has seen a flurry of projects and an average startup time of around 5.5 years, Cyprus and Namibia are still awaiting first oil and gas production.

Cronos gas field is anticipated to be the first of the Mediterranean fields online, targeting a 2028 startup. However, an anticipated FID deadline of 2025 was missed, with a new target of late 2027–early 2028 for startup mentioned by the field operator.

Six years from discovery would still mark a rapid development — unlike the Aphrodite field. Cyprus’ first discovery from 2011 just reached start front-end engineering design (FEED) work at the end of 2025, and is targeting first gas 20 years after discovery in 2031. Development of a new LNG export network was deemed “economically unfeasible,” rather Cyprus is planning to leverage its proximity to Egypt and tap into that network.

In Namibia, Venus oil field propelled conversations of the “hotspot” Orange Basin. However, many challenges in developing the project exist, including its depth and distance from shore which make it one of the “most technically demanding offshore projects in the world.” Shell’s announcement that it is not intending to direct major new funding to the country leaves development of infrastructure on TotalEnergies, driving up costs and potentially delaying development.

Fast-tracked developments

With increased focus and capital, fast-tracking of developments is possible under narrow circumstances. For instance, Pemex brought its Bakté field online at a “record-breaking” pace within twelve months of discovery. However, Bakte employed a strategy of “early production,” meaning just the first of six production wells were completed at the time of first shipment to market. Pemex’s strategy of early production has allowed the national oil company (NOC) to begin production “without presenting a formal, thorough development plan” by producing from testing infrastructure, leading some experts to question the practice.

In Guyana, ExxonMobil has also been able to rapidly develop new fields. Liza was the country and Exxon’s first discovery, made in 2015, and the field began production in 2019. An Exxon executive posted, “That short timeframe — less than five years! — is nearly unheard of in our industry. On most deepwater developments, it typically takes twice as long to safely extract the first commercial barrel.” However, the speed of discovery to extraction prompted questions into government promotion of extraction, as well as litigation over permits, insurances, and constitutionality. So while Exxon and partners did get the project up and running quickly, assertions of relaxed government enforcement and “accusations of environmental abuses” may endanger the long term viability of the project.

Decline rates, stranded assets, and the climate

The IEA declared “the oil and gas industry needs to run fast to stand still” in its 2025 analysis of field decline rates. That report made similar points about long lead times, but took them as indication that investment is needed now in order to ensure future demand is met. This approach assumes a level of future gas demand that is likely unwarranted and locks in future gas use that would violate many countries' stated objectives.

Maintaining current production levels would put 2050 production levels higher than what is included in the IEA’s Stated Policies Scenario (STEPS), which equates to warming of around 2.6°C by 2100. The Production gap report reaffirms that “supply and demand must decline rapidly and substantially between now and mid-century” to limit warming to 1.5°C — the primary temperature goal under international law. Investment in new oil and gas is either an investment in climate destruction or in stranded assets.

The IEA net zero emissions scenario does not call for an “absence of investment,” rather for significantly reducing it. The complexity of new projects means that there will be many years before startup, so investing now is locking in the future, either betting on overshoot or stranded assets. The same long lead times cited as a reason to invest now are precisely what make such investment dangerous under climate uncertainty.

Conclusion

Developing oil and gas fields has always been a complicated and risky endeavor, but in recent years it has become even more so, as evidenced by the time companies need to develop new projects. This trend is likely to continue, as easier projects are developed first, and the remaining ones become more difficult to exploit.

This does not mean that companies will cease putting dangerous projects online. In the coming years, companies are targeting, investing in, and starting up projects that look very similar to the 2025 start-ups described here and are likely to face many of the same issues.

Investment in new oil and gas projects is betting on climate disaster and endangering ecosystems. Spending should be directed away from projects betting against the future and toward demand reduction and renewable energy, which have the potential to bring in genuine energy security.

About the Global Oil and Gas Extraction Tracker

GOGET is an information resource on gas oil extraction projects. The internal GOGET database is updated continuously throughout the year, and the annual release is published and distributed with a data download, summary tables, and unit wiki pages. The data are released under a creative commons license. Commercial datasets exist but are prohibitively expensive for many would-be users. Global Energy Monitor developed GOGET so that high-quality data on these projects is available to all.

Media Contact

Scott Zimmerman

Project Manager, Global Oil and Gas Extraction Tracker