New data in the Global Oil Infrastructure Tracker show the continuing global expansion of crude oil transmission pipelines. Asian and African countries lead the buildout, particularly in the Middle East, though the U.S. is developing key projects to maintain its foothold as one of the top exporters.

The buildout of oil pipelines continues at a global scale, according to the May 2024 Global Oil Infrastructure Tracker (GOIT) data release from Global Energy Monitor. In total, the world is constructing nearly 11,000 kilometers (km) of crude oil transmission pipelines — about the length of the Earth’s diameter — with an additional 22,700 km proposed. Compared to the same time last year, this represents an 8% increase in total km in development.

The infrastructure currently under construction is estimated to cost US$25.5 billion in capital expenditure, and the additional proposed km would add US$106.2 billion more. The lion’s share of costs will fall on Africa and Asia, who lead the buildout.

Some regions are building pipelines with the goal of becoming exporters, like coastal sub-Saharan Africa countries. Elsewhere, major importers like India and China are adding pipelines to existing networks to serve refineries and petrochemical complexes. But some of the more consequential buildouts are happening in traditional oil production regions like the Persian Gulf in Western Asia, and the U.S. and Canada in North America, who are expanding to maintain their foothold as global oil exporters. Many of these pipeline buildouts are led by state-owned companies, though others like France’s TotalEnergies and the U.S.’s ConocoPhillips are in the mix.

The fervor for oil exports is exemplified by developments in North America, in particular along the U.S. Gulf Coast. While the U.S. isn’t leading the global buildout by km or costs, these shorelines are already a major global export hub, with terminals and refineries processing crude oil and other liquids from the Permian basin and the Cushing, Oklahoma storage hub to send them abroad.

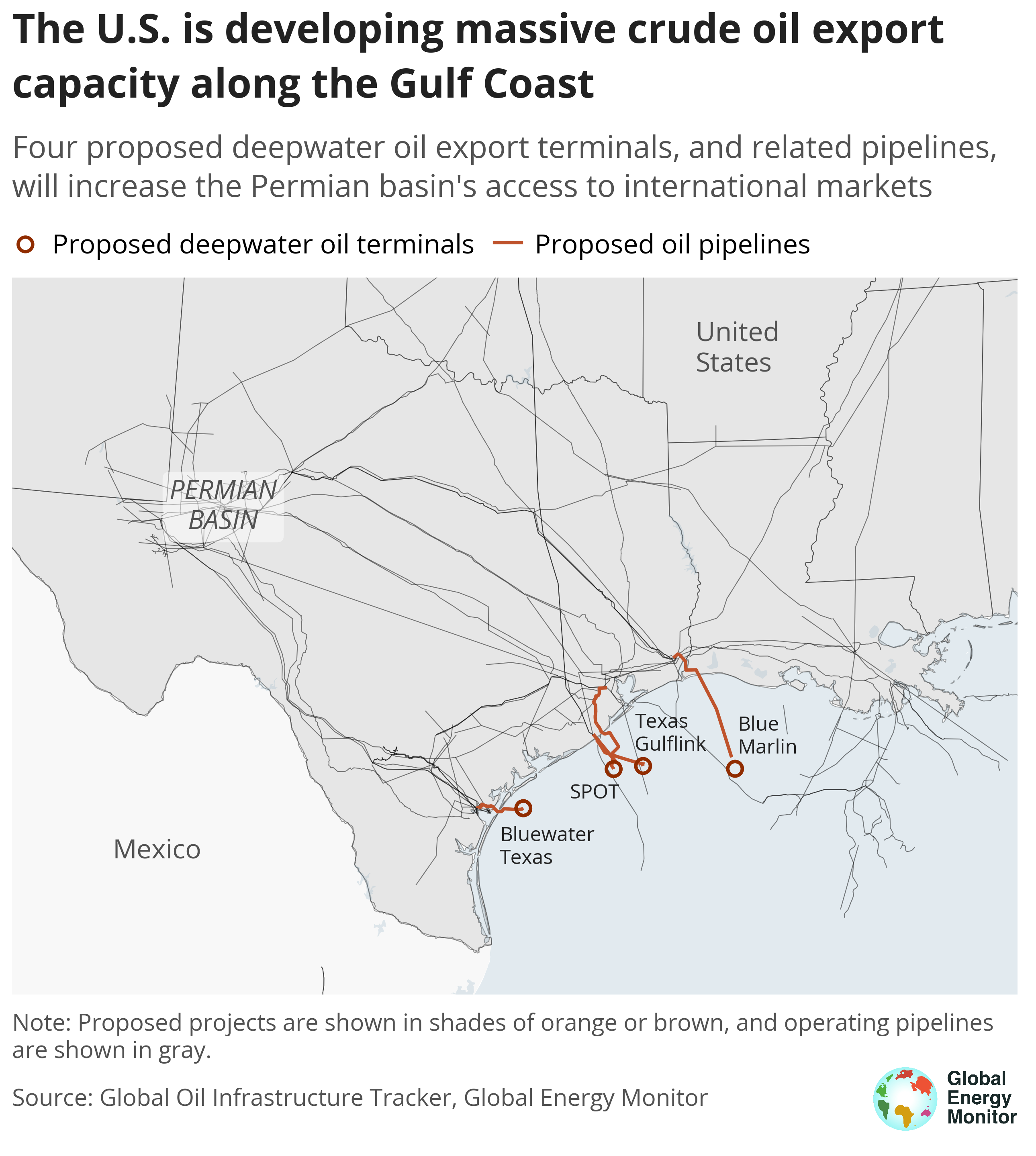

Last year, the U.S. hit record oil production and export numbers, and this year, the trend is expected to continue, with recent forecasts of even higher production. But the Permian’s takeaway capacity — the volume of oil and gas it can export now with existing pipeline infrastructure — is near its limit and may be maxed out by the end of 2024. Thus, each new pipeline and expansion project adds only marginal takeaway capacity that producers bank on. Currently, seven major projects are in development to reduce that constraint, four of which connect directly to proposed oil export terminals.

There are four crude oil export terminals currently in development off the Texas and Louisiana coasts, each of which would be able to dock giant crude carriers and export up to two billion barrels of oil per day. The most imminent is Sea Port Oil Terminal (SPOT), which in April 2024 was issued a deepwater port license by the U.S. Maritime Administration (MARAD).

In the U.S., the development of pipelines and export terminals will continue to move in tandem. Additional export capacity will spur further oil production, and the oil production will be accompanied by increased gas production, as the majority of gas produced in the Permian is associated gas (meaning it is found with petroleum deposits and comes out of the ground alongside oil). The recent pause on liquefied natural gas (LNG) export approvals by the Biden administration has been a temporary obstacle in the global LNG export race. But because much of Permian gas is associated, approving and building oil export terminals could erode any case for further pausing or rejecting LNG export capacity. The oil and gas have to go somewhere.

At a time when scientists agree any additional fossil fuel extraction will cause unsafe levels of climate warming — and in a geopolitical context where additional fossil fuel exports out of the U.S. decrease energy security everywhere by increasing energy price volatility at home and abroad — expansions like this are climate-damaging bets on an uncertain future.