Key points

- 216 gigawatts of green hydrogen projects are proposed in 11 countries in Africa, but it’s unclear if the projects are technically or financially feasible.

- 61% of all prospective utility-scale wind and solar projects on the African continent are for green hydrogen — primarily slated for export to Europe, which has yet to establish a market for it.

- Small, distributed wind and solar projects have proven effective in addressing energy access in Africa, with millions of Africans benefiting from these projects; meanwhile, hydrogen remains largely hypothetical.

Africa has the vast potential to develop wind and solar energy, but much of its future capacity is not intended for domestic consumption, but rather export to Europe in the form of “green” hydrogen, according to a new analysis from Global Energy Monitor (GEM). The feasibility of these projects faces strong headwinds, ranging from a lack of funding and offtakers to unrealistic timelines and technological hurdles, suggesting these large projects won’t be economically viable, even if they are built.

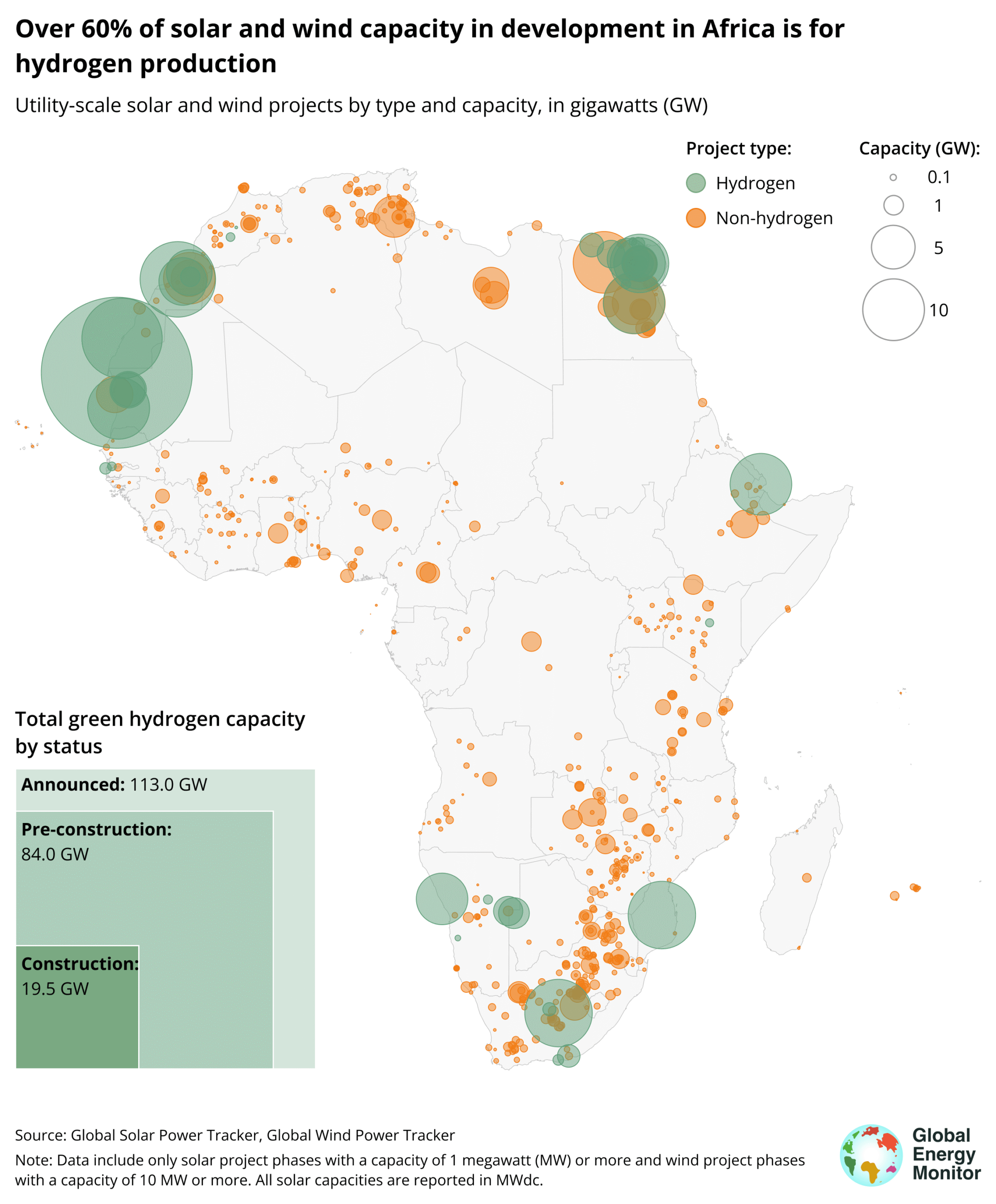

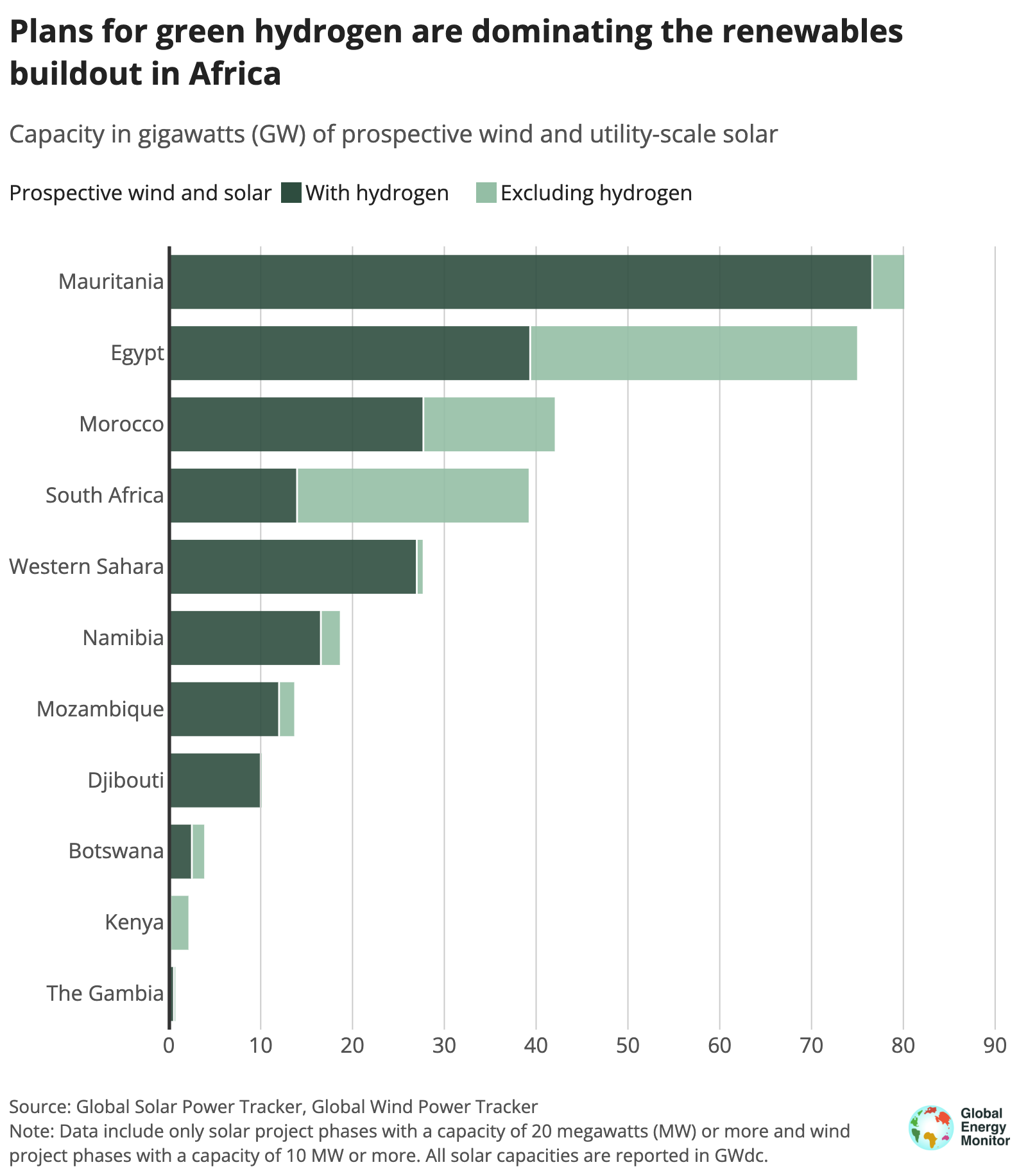

Data in the Global Wind Power Tracker and Global Solar Power Tracker count roughly 350 gigawatts (GW) of prospective utility-scale wind and solar capacity across Africa — that is projects that have been announced or are in the pre-construction and construction phases — roughly ten times what is currently in operation across the continent. By comparison, the entire world installed 380 GW of solar in the first half of 2025. But nearly two-thirds of Africa’s proposed renewables capacity, 216 GW across 35 projects, is planned for use in “green” hydrogen production, the majority of which is designated for export rather than remaining in Africa for domestic use. These projects, sometimes hundreds of times larger than the host country’s current wind and solar capacity, pull investment and resources from international decarbonisation efforts, like the goal of tripling of renewables by 2030 that was agreed at COP28. They also pull resources from projects on the other end of the spectrum that can have immediate positive impacts, with projects as small as 50 kW (0.00005 GW) holding the potential to increase local household incomes by two-thirds.

In eleven African countries/areas — Botswana, Djibouti, Egypt, Kenya, Mauritania, Morocco, Mozambique, Namibia, South Africa, The Gambia, and Western Sahara — the promise of becoming green hydrogen hubs and exporting that hydrogen as fuel or industrial feedstocks to Europe has spawned some of the largest proposed energy infrastructure in the world. However, the companies that are promising to build this infrastructure, the majority of which are European entities, have never built on this scale before, and the export market does not yet exist. Companies and governments promoting green hydrogen on the continent need to be transparent about the gamble they are taking and ensure that where hydrogen projects are proposed, people have as much autonomy as possible to decide what type of energy and exports are best suited for them.

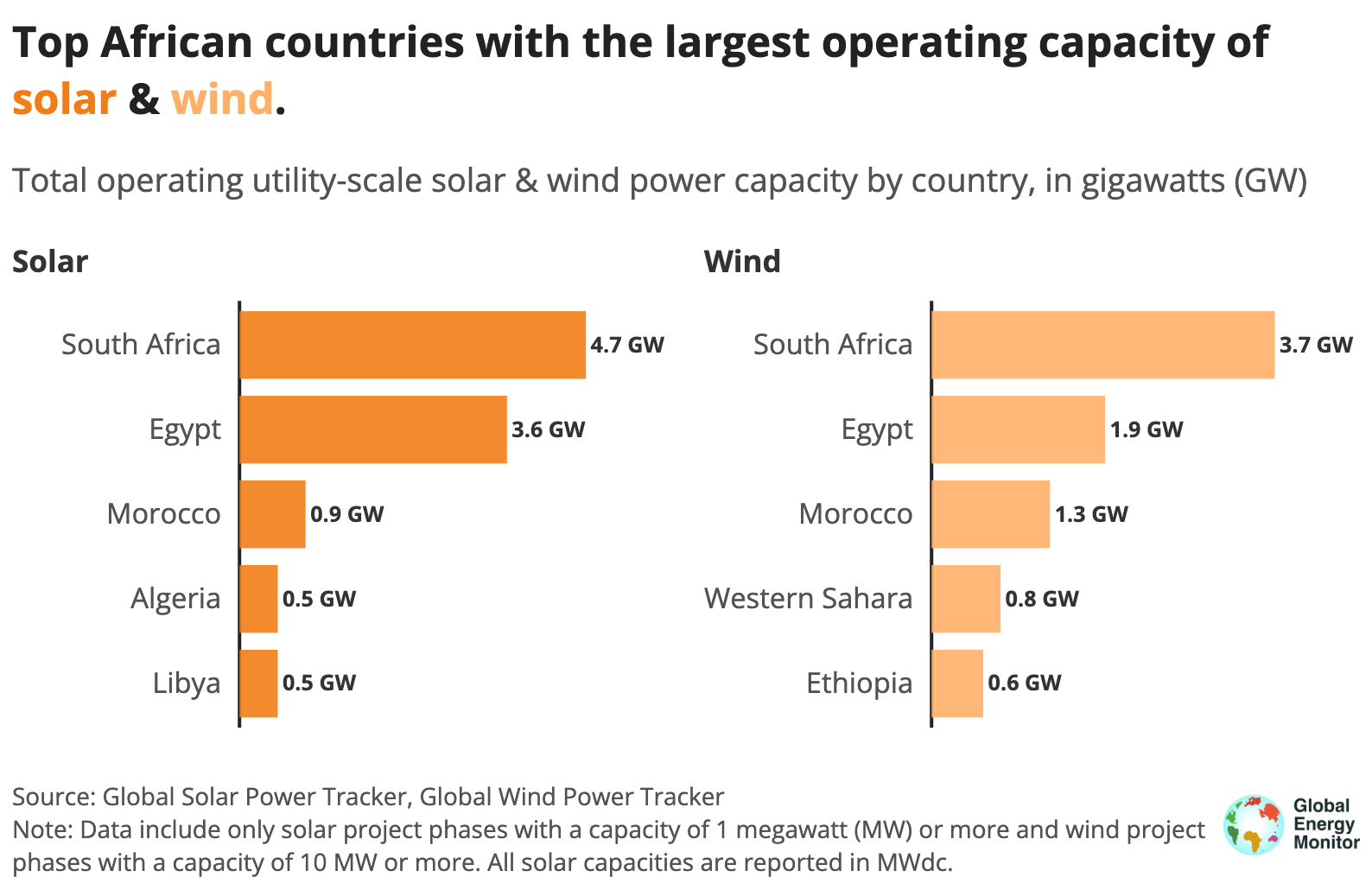

Figure 1

Hypothetical Hydrogen

Global Energy Monitor’s comprehensive coverage of renewables on the African continent paints a picture of large green hydrogen projects being developed in countries that currently have extremely limited energy access for their populations. The term “green” hydrogen refers to any hydrogen or hydrogen-related product, such as ammonia, that is produced using electrolysis specifically powered by renewable energy. Typically these projects are designed to run on wind, solar, or occasionally hydro power. Because Europe has struggled to meet its renewable energy commitments and emissions goals, some countries are attempting to capitalize on Africa’s abundant renewable energy potential.

Table 1

Beyond Europe and Africa, the global capacity of green hydrogen used specifically for power generation was a mere 0.4 GW in 2024, according to the International Energy Agency. This is dwarfed by most prospective African projects, which on average are fifteen times larger at 6.2 GW.

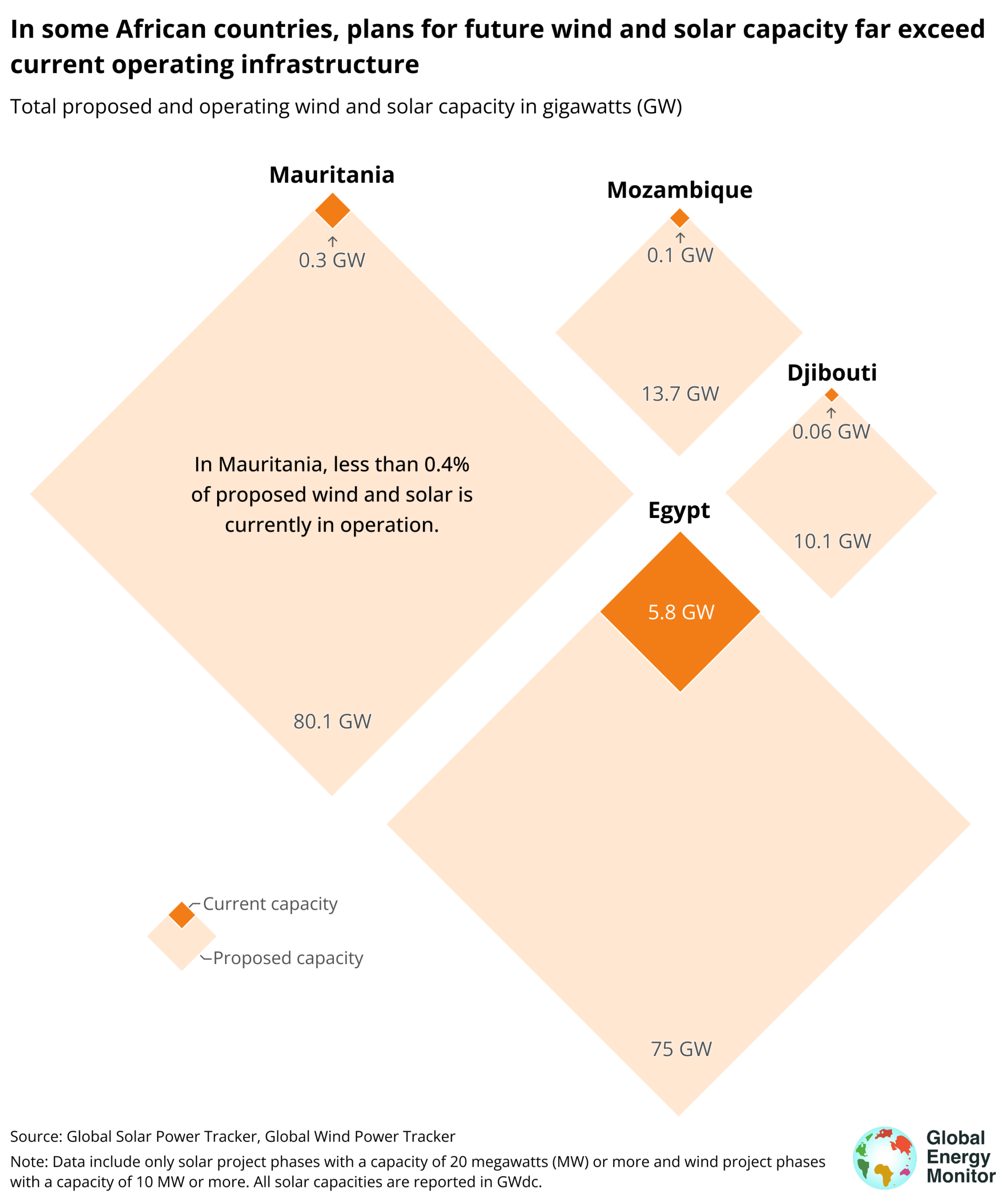

Mozambique and Djibouti have almost no renewable energy infrastructure — 0.1 and .06 GW respectively, or enough capacity to power roughly 50,000 European households — and yet there are plans to build twelve and ten GW of green hydrogen infrastructure in each country, respectively. If the twelve GW project in Mozambique was instead used to provide electricity, it would double the amount of power the country is currently generating. With its much smaller population, Djibouti could have equivalent per capita electricity consumption to Europe with just three GW of wind and solar.

In more industrialized countries such as Egypt, which already has 5.8 GW of operating wind and solar, the country plans to boost its total wind and solar capacity by 39.3 GW with green hydrogen projects. The scale of projects is the most unrealistic for companies proposing infrastructure in Mauritania, with 79.5 GW of announced wind and solar, all of which are set to produce hydrogen. Mauritania only has 0.3 GW of wind and solar in operation, or less than 0.4% of what is proposed. Put another way, a nation with only 0.3 GW of utility-scale wind and solar in operation has plans from multinational developers to build infrastructure 3.4 times the capacity of the current largest energy project in the world, the Three Gorges Dam in China at 22.5 GW.

Figure 2

In addition to their unprecedented size, fewer than half of the green hydrogen projects in Africa have timelines for completion, making it unclear when they would actually come online. Msenge Emoyeni wind farm, at 0.07 GW, is the sole green hydrogen project currently operating in the continent, while 52% (113.0 GW) of hydrogen projects are announced and only 9% (19.5 GW) are under construction.

For a country like South Africa, solar projects take an average of four years to build while wind can take roughly five-and-a-half, though these are timelines for projects at smaller scales than the proposed green hydrogen. The country’s current largest operational solar project is 0.5 GW, and the largest wind projects only reach 0.1 GW.

Two projects, Guelmim Green Hydrogen and Prieska Power Reserve, were supposed to come online in 2026, but neither are under construction as of October 2025. Only one of the fourteen projects slated to come online by 2028 is under construction, the 2.1 GW solar phase of the hybrid Voltalia-TAQA project. The largest proposed project on the continent, Megaton Moon, is estimated by GreenGo to come fully online by 2035. All other projects, representing 133.9 GW, do not list a timeline for completion.

Figure 3

Lack of offtakers

If any of these projects do come online, it remains unclear who would be the offtakers, or parties who have committed to buy the hydrogen. Of the 35 green hydrogen projects GEM tracks in Africa, only four have public announcements of offtake agreements with specific buyers. Because of the lack of consumers, Germany’s hydrogen strategy states that it would likely have to increase carbon taxation to force the market to shift in order to make imported hydrogen economically viable. Germany’s plans only include ten GW of domestic green hydrogen production, though Germany in particular has leaned heavily into imports as a strategy to meet its renewable energy goals, making it a key pillar of its National Hydrogen Strategy. One of the largest projects planning on exporting to Germany is the 30 GW AMAN project in Mauritania; CWP Global initially stated that the project was expected to raise the African nation’s GDP by 40–50% by 2030 and 50–60% by 2035. Instead, the project has been paused indefinitely due to a lack of offtakers.

Despite the hype, the market has largely failed to make demand for the product. These projects also rely on the assumption that consumers in Europe will be willing to make the switch to hydrogen-capable technologies, though this has really only been seen in the heavy industry sector, not for widespread domestic energy use. Where hydrogen is planned in industrial applications, major steelmakers have delayed investments and started to walk back green projects, signaling a weak market for green hydrogen imports.

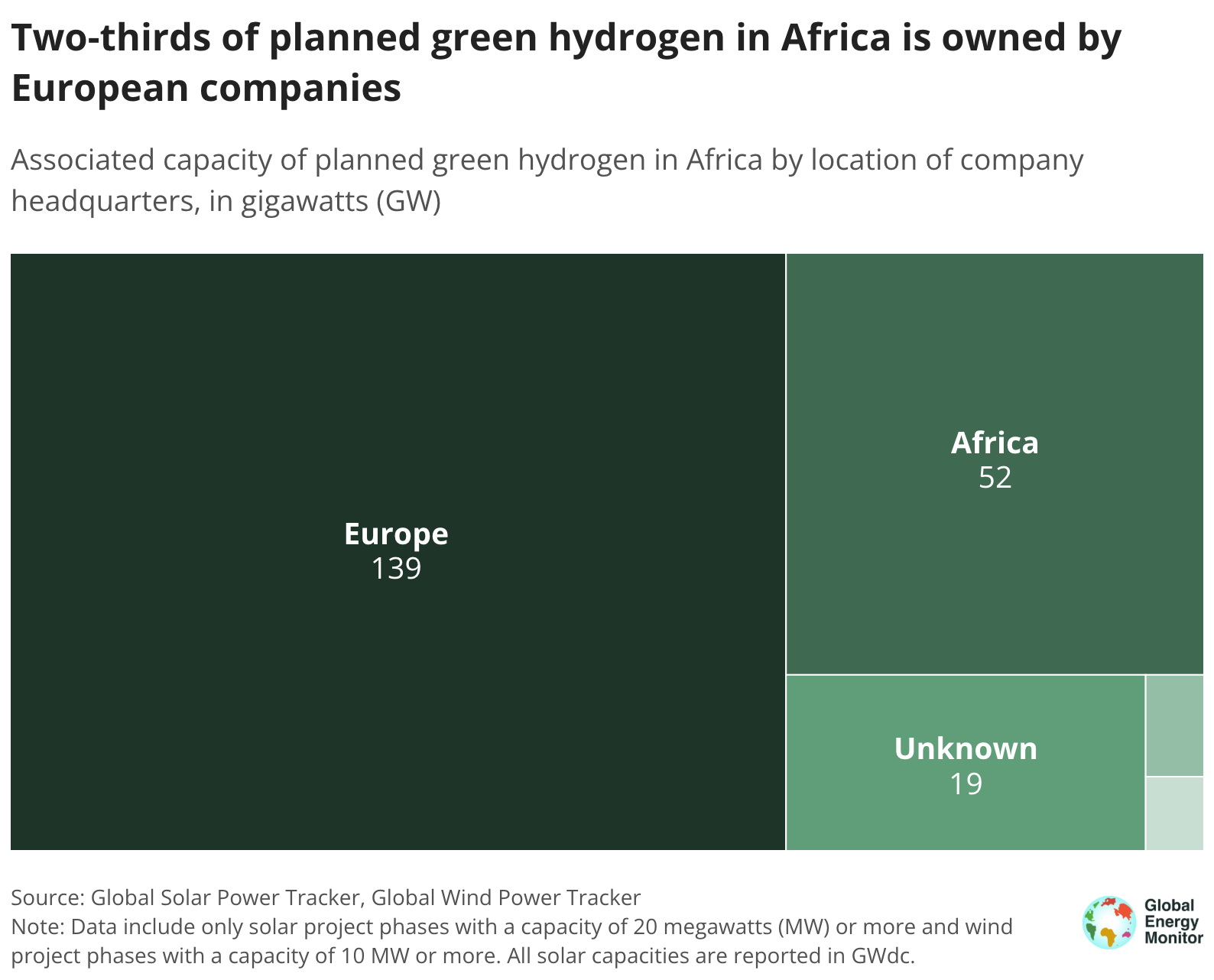

Aside from the Danish GreenGo, which owns the 60 GW Megaton Moon, GEM data show that CWP Global has historically been the biggest player in African green hydrogen, with 41.1 GW planned. Of the prospective green hydrogen projects in Africa, 65% are European-owned and only 25% African-owned. Furthermore, the majority of revenue in the hydrogen value chain is wherever the end user purchases it; therefore, if the bulk of the planned green hydrogen is exported, these projects provide little value to African countries. For projects that would produce green hydrogen for use in heavy industry, such as steelmaking, more value could be preserved locally if countries produced green iron for export instead. Mauritania, South Africa, and Egypt are already major producers of iron ore.

Figure 4

Funding strategies for large projects also remain unclear. Historically, resource extraction from Africa to Europe has left African nations saddled with inescapable foreign debt, which also makes local ownership of assets difficult. To add to this, funding from both the private and public sector often falls short in Africa; in 2021, energy investment per capita in Europe was 41 times greater than Sub-Saharan Africa. The African Development Bank (AfDB) had the aspirational goal of achieving universal electricity access by 2025, however AfDB only procured $12 billion USD total of the estimated $60–90 billion per year that was needed. The multilateral initiative, Mission 300, aims to give access to 250 million Africans by 2030 and has provided access to electricity for 32 million since 2023, although it still requires significant further investment.

Lack of infrastructure

For most of these countries, especially in Sub-Saharan Africa, transmission systems such as pipelines and electrical transmission lines are lacking or entirely nonexistent. Combustion fuels like coal, oil, gas, and hydrogen, built at the utility scale, either require they be utilized close to the source of that power, or necessitate sprawling and disruptive transmission systems spanning entire countries, while very small-scale projects do not. In addition, the farther away from the source of hydrogen production that the fuel is transported, the less energy efficient and cost effective it becomes. Most existing pipelines would need to be overhauled, as these pipelines are currently built to keep hydrogen out. Establishing local industry, which can use hydrogen on site, such as green iron and green fertilizer, would preempt the need for novel infrastructure while boosting local economies.

Without pipelines, transportation of hydrogen to Europe would require a tremendous effort around shipping, an expensive endeavor: One study found that only two percent of the 10,000 locations studied for export to Europe were cost competitive. Neither export nor import infrastructure to handle hydrogen transportation has yet to begin construction, while much of the infrastructure proposed seems fated to prolong the life of existing fossil fuel networks. Pipelines also pose the issue of becoming stranded assets with hydrogen infrastructure investments needing both import and export markets to surface and remain stable long term.

Projects that fail to deliver

Smaller projects such as solar minigrids are already feasible and are proven to support African electrification. Energy access has improved in recent decades, but has stagnated since 2020 even where fossil fuels are being used, leaving hundreds of millions unconnected. Electricity is an important and urgently needed driver of economic growth, giving opportunities to impoverished communities. Currently, developers are limiting local people’s ability to advocate for themselves by using minimal environmental standards and failing to make input on environmental impact studies accessible. For communities facing exploitation for hydrogen, a common slogan has been “Africa is not Europe’s battery.”

While there are examples where a balance between the energy needs of hydrogen production and the energy needs of communities has been sought, these projects still heavily favour hydrogen. In South Africa, the Northern Cape Green Hydrogen Strategy plans for ten GW of renewables, five GW of which would be used for hydrogen production. Under this plan, 70% of the energy produced would go towards hydrogen exports and only 30% would remain locally. Hydrogen production is also water-intensive: Producing one kilogram of green hydrogen requires up to 30 liters of fresh water, which risks depleting local water supplies. For regions like South Africa, some developers have tried to tackle the local water and energy issues by planning to use only desalinated sea water.

Namibia’s seven GW Duares Green Hydrogen Village similarly mentions ocean water as a solution. The company has also ventured to ensure 10% of the project’s shareholders are local community groups, and 50% of workers are slated to be from the Daures area as well. Still, the project developer, Hyphen, was denied use of Shark Island as part of its export infrastructure due to its cultural significance, with a genocide taking place there in the early 20th century, and reparations still not made by Germany. Infrastructure like this is consistently delayed or loses funding: in September of 2025, German power utility RWE pulled $10 billion in funding from the Daures project.

In Tunisia, where just 0.3 GW of wind and solar are operational, the German Agency for International Cooperation backed the expansive Tunisian Hydrogen Strategy. Specific green hydrogen projects have not yet been announced, but the strategy plans to use 248 million cubic meters of desalinated water by 2050, equivalent to the consumption of half the population, in one of the most water-scare nations in the world.

Projects at workable scale

Figure 5

Existing utility-scale solar and wind in Africa provides examples of how smaller-scale projects are proving successful. Burundi’s first solar farm, a mere 0.008 GW, increased the country’s energy supply by over 10% and made Mubuga the first capital city in the world powered by solar during the day. In Mauritania, less than 50% of people and just over 3% in rural areas have access to energy; however, AfDB has provided funding for seven remote “minigrid” projects that run on solar combined with diesel, which would electrify 40 rural communities. Meanwhile, plans are being drawn up for a staggering 76 GW of green hydrogen, yet only 0.2 GW of solar and 0.1 GW of wind currently exist; planned hydrogen would be 255 times the size of this current capacity. AMDA, a coalition of 61 companies across 24 countries, has successfully deployed minigrids across the continent, giving electricity access to one million people so far, with 600 projects successfully built.

In KwaZakhele, South Africa, residents were unable to run their businesses or study for school after dark due to blackouts, so the "Saltuba Cooperative" built a 5 kW (0.000005 GW) solar installation on a carport. A group of 36 homes created a pilot project to produce, manage, and potentially create an income stream selling this electricity to the municipality. Researchers from the South African Labour Bulletin assert that if the project were scaled up to 50 kW, it would be able to raise the average household income in the municipality by nearly two-thirds.

Africa needs an estimated 160 GW of energy to provide electricity for the roughly 600 million Africans who do not yet have access, and small, distributed projects have proven pivotal. Africa’s immense potential for wind and solar projects can provide energy access and economic opportunities. GEM tracks 139 GW of utility-scale solar and wind projects that would provide clean electricity throughout the continent if the funding and backing can manifest, but those projects need solid footing, which hydrogen hasn’t yet proven itself to have.

About the Global Solar and Wind Trackers

The Global Solar Power Tracker is a worldwide dataset of utility-scale solar photovoltaic (PV) and solar thermal facilities. It covers all operating solar farm phases with capacities of one megawatt (MW) or more and all announced, pre-construction, construction, and shelved projects with capacities greater than 20 MW. The Global Wind Power Tracker is a worldwide dataset of utility-scale, on- and offshore wind facilities. It includes wind farm phases with capacities of ten MW or more.

Supplementary information on the Methodology used for this brief can be found on our Methodology wiki page.

Media Contact

Julie Macuga

Senior Researcher, Global Energy Monitor