Prague, CZ – In spite of official targets aimed at slashing EU gas demand, European countries plan to double the bloc’s liquefied natural gas (LNG) import terminal capacity in response to Russian gas supply disruptions, finds new research from Global Energy Monitor (GEM).

GEM data show that, taken together, these project proposals threaten to derail EU climate goals while doing little to address the energy crisis, as most of the LNG contracts secured by EU buyers so far are set to start from 2026 and continue for 15 to 20 years.

Since Russia’s invasion of Ukraine, 195 billion cubic meters (bcm/yr) in LNG import terminal capacity has been announced to come online by 2026 at a minimum cost of EUR 7 billion, data from the Europe Gas Tracker shows. Prior to the war, GEM’s Global Gas Infrastructure Tracker shows, the EU’s operating import terminals had 164 bcm/y of available regasification capacity. By comparison, the EU imported 155 bcm of gas in 2021 from Russia, including LNG.

Under the European Climate Law, the EU aims to reduce gas demand by 35% compared to 2019 levels by 2030, while the Commission’s REPowerEU proposal from May this year could entail a 52% reduction in EU gas demand by 2030.

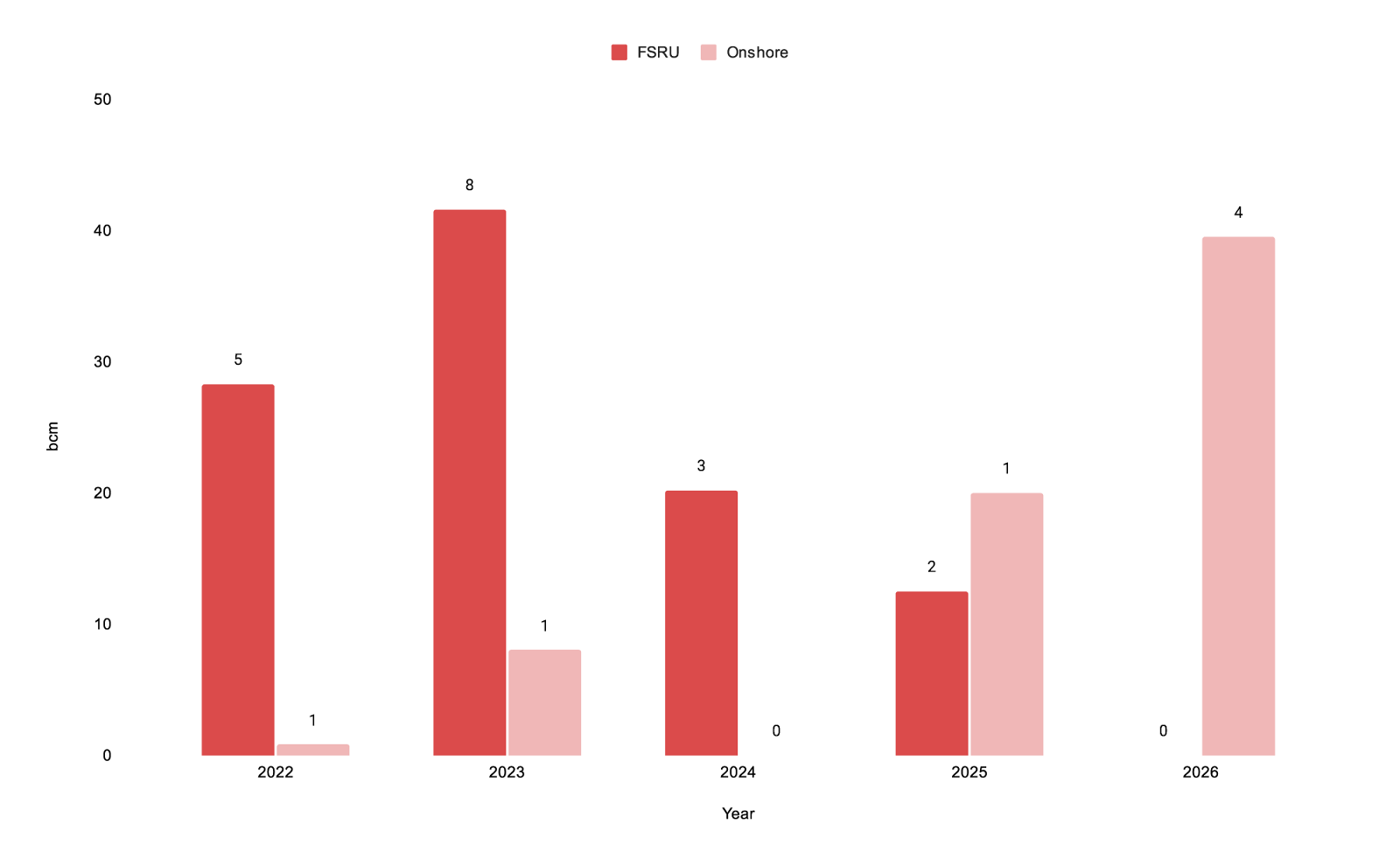

GEM research as of 5 December shows:

- 9.1 bcm/y of new capacity has already started operating at Krk FSRU (Croatia), Revithoussa LNG Terminal (Greece), and Eemshaven FSRU (Netherlands);

- 33 bcm/y of capacity is under construction and expected to be operating in 2022 or early 2023 at El Musel (Spain), Inkoo (Finland), and Brunsbuttel, Lubmin, and Wilhelmshaven (Germany);

- Seven proposed import terminal projects are projected to begin operating before the end of 2023 with potential capacity of 36.6 bcm/y. Four of these are floating terminal projects along Germany’s northern coast.

- Other proposals, if realised, would take the overall crisis capacity boost to 195 bcm/y by 2026. In addition, the Dutch government has said this month it is looking at ways to further boost regasification capacity following the commissioning of a new floating terminal already this year. [3]

Greig Aitken, Project manager of the Europe Gas Tracker, said, “An awful lot of time, money, and cutting of environmental guardrails has gone into Europe’s big LNG capacity bet this year. Limited and expensive global LNG supply remains the fundamental problem that these new projects cannot overcome in the short-term.”

“When supply tightness eases in 2026, this excessive capacity infrastructure would need to be used to avoid becoming stranded assets, but by doing so Europe’s climate goals will be put in jeopardy as they require substantial cuts in gas consumption.”

Capacity and number of planned floating storage and regasification unit (FSRU) and onshore projects by year

Contact

Greig Aitken, Europe Gas Tracker project manager, Global Energy Monitor, [email protected]

Notes for editors

- See the GEM briefing ‘When is enough, enough? The state of play with Europe’s new LNG terminal projects in response to the energy crisis’

- Twenty-six European LNG project proposals have appeared since February this year (see spreadsheet), comprising new projects, older projects which had been canceled, and capacity expansion projects at existing terminals.

- See LNG Prime, December 1, 2022